If you want to stay out of jail then you have to pay your taxes.

But there is no reason to leave a tip.

And making mistakes with TSP withdrawals is a great way to leave the government a tip.

So before taking a TSP withdrawal then you are going to want to read this article.

While Tied to The Desk

Tax planning in retirement is important but if you are still working then here are the 3 main things that could affect your taxes now.

If you are already retired, jump to the retired section below.

Traditional Vs. Roth TSP

While working you can decide to contribute money to either the Roth TSP or the Traditional TSP.

If you do traditional then you lower your taxes now but pay the taxes in retirement. With the Roth you don’t get a tax deduction now but never have to pay taxes on it later.

This article here will help you make a decision between the two.

HSA/FSA

These accounts can have triple tax savings while paying for things you would pay for anyways.

You can check out the details here.

Charity/Mortgage Interest

People often think they get more tax benefit from these things than they actually do.

To get any tax benefit from giving to charity or your mortgage interest then you would have to have enough deductions to itemize your deductions.

In other words, you’d have to have more itemizable deductions than the standard deduction which is not the case for most people.

While Retired

While retired here are the big things that affect your taxes.

TSP Withdrawals

Whenever you take money out of the traditional TSP then you must pay taxes on it.

For example, if you take $20,000 out then $4,000 will often be automatically withheld and sent to the IRS.

Watch Out!!

While working it is difficult to do any one thing that causes a huge tax problem.

However, people cause major tax problems in retirement all the time.

This is simply because huge spikes in income are rare while you are working but while retired huge spikes in income can be created when you make a large TSP withdrawal.

The reason this is such a problem is because many people pay $10,000’s+ in extra/unnecessary taxes to the government because of these spikes.

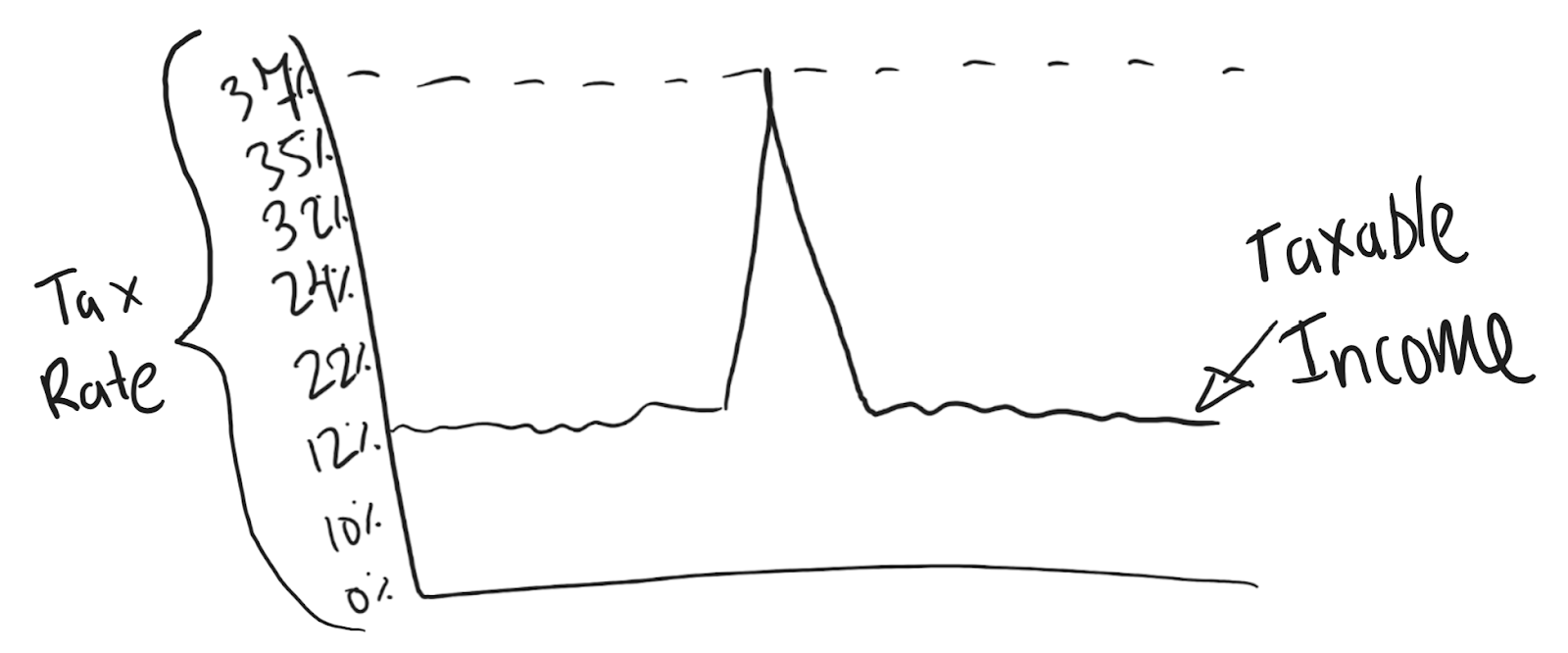

Here is an example to show my point:

Let’s say you need a large amount of money from your TSP for a large retirement purchase.

This could be paying off the mortgage, buying a boat, etc.

A spike in income may look like this (See picture above).

This person may normally be in the 12% tax bracket but would be shoved into a much higher tax bracket because of the big withdrawal.

This means that they’ll have to pay much more than 12% of that big withdrawal to the government.

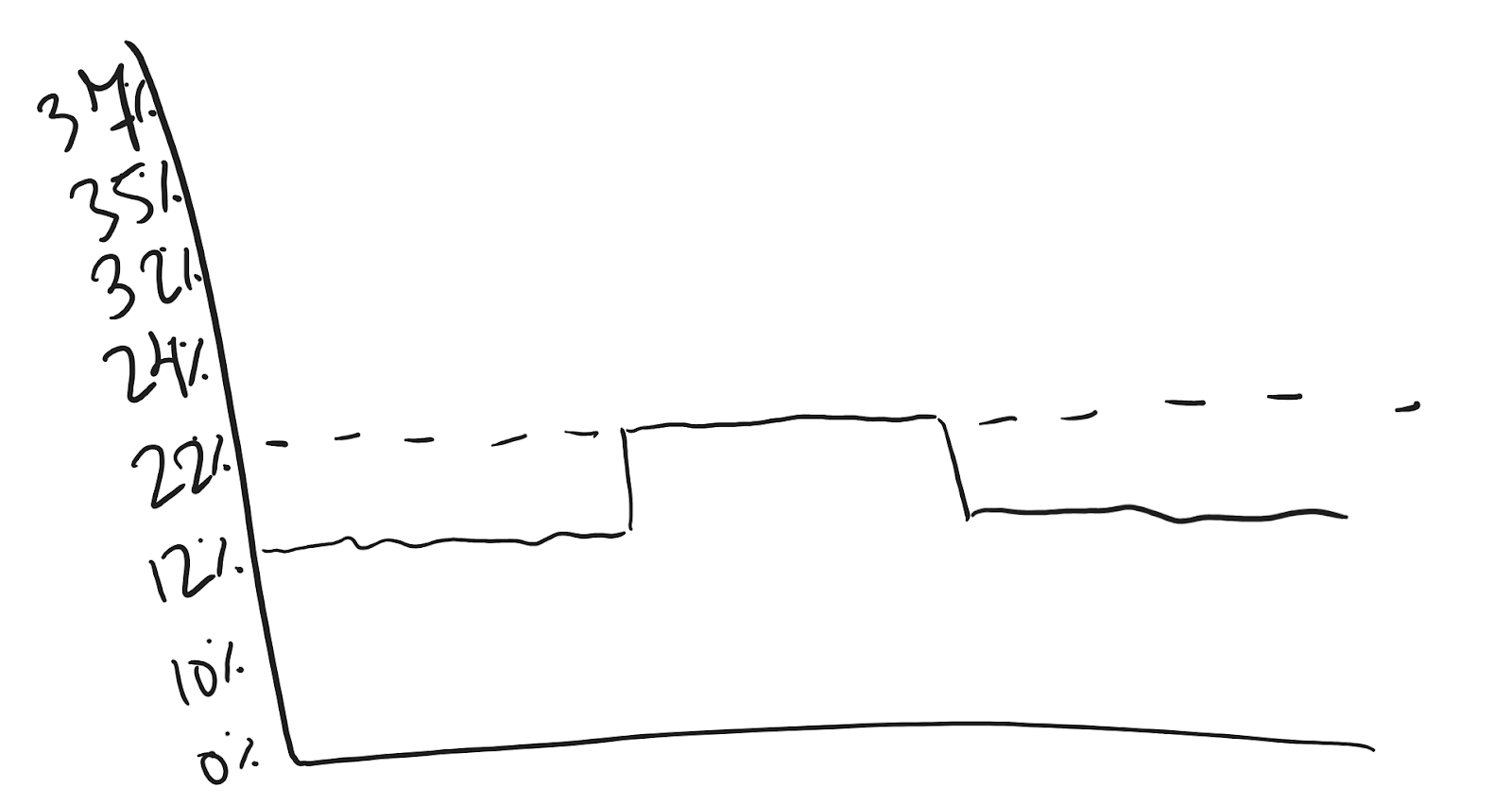

Even if someone wanted to withdraw the same amount of money it would be much better to spread that withdrawal out over years.

It could look something like this:

In this example (above), their tax bracket does go up but not nearly as much as the withdrawal is spread out over time.

Know your Tax Bracket!

So before you take a withdrawal from your TSP you are going to want to have an idea of what tax bracket you’re in.

That way you’ll know what a TSP withdrawal will do to your tax bracket and how much you can withdraw before going into a higher bracket.

This becomes even more important as the size of the withdrawal goes up.

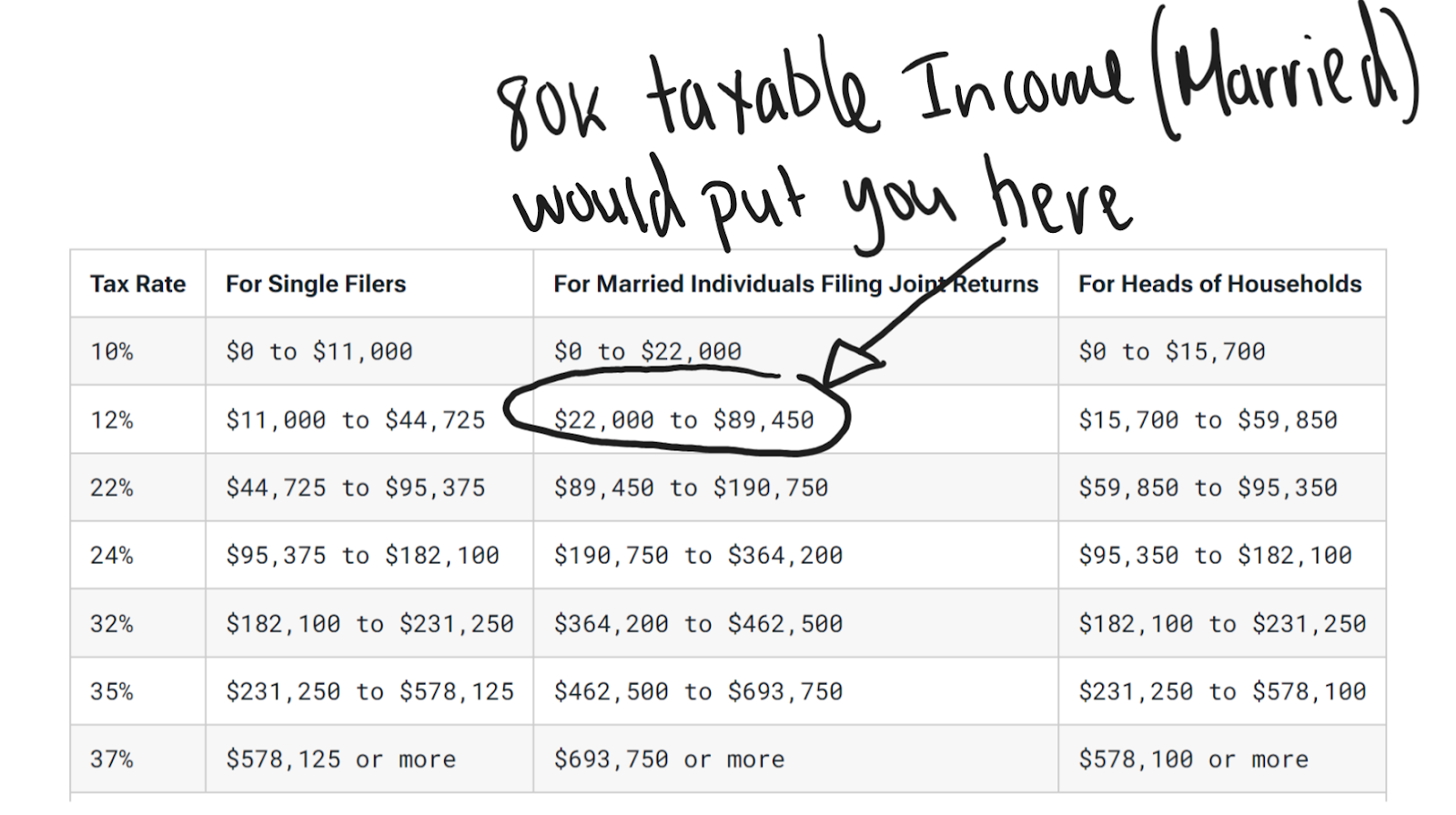

For example, if you are married and have 80k in taxable income (in 2023) then you’d be in the 12% tax bracket (See picture below).

But once your taxable income goes over $89,450 then you’d be in the 22% tax bracket! That is a 10% jump in taxes!!

Income Means Taxes

But we have to remember that taxes are not all bad.

If you are paying taxes then that means that you have income and we all like income.

The most important thing is to understand at least the basics of how taxes work so you don’t give more than you have to to the government.