Who is Eligible for a MRA+10 Retirement?

There are two main criteria to be eligible for a MRA+10 retirement.

You have to have met your MRA (minimum retirement age) and you have to have at least 10 years of creditable service.

Note: At least 5 years of your creditable service has to be civilian service time and not military service that you bought back.

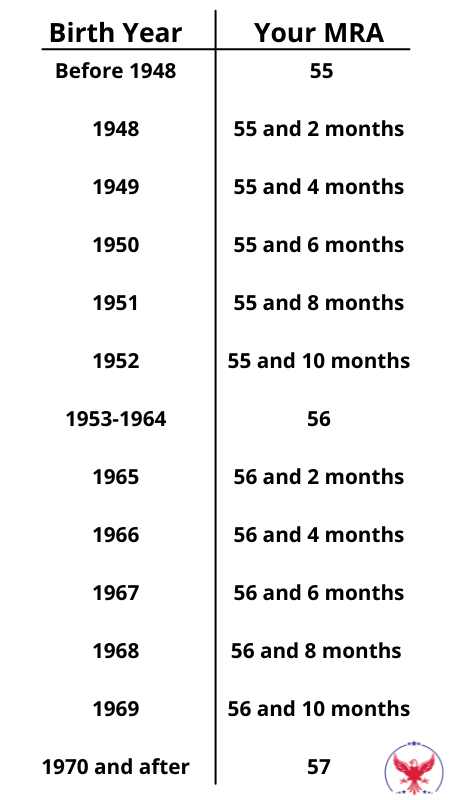

Your MRA is based on your birth year per this chart.

If you have met your MRA and have at least 10 years of creditable service then you are eligible for a MRA+10 retirement! The next important thing to understand is what benefits you get (and don’t get) under this type of retirement.

How to Calculate Your MRA+10 Retirement Pension

The first step to calculating the pension for a MRA+10 retirement is the same as other types as well.

You take your creditable years of service and multiply it by your high-3 (average annual salary for the 3 years of your career you got paid the most) and your multiplier which would be 1% for this type of retirement.

Once you find your gross annual pension with the above formula then you have to think about the reduction for taking the MRA+10 retirement as I’ll show in the examples below.