Some people are 100% content with doing their 30 years with the government, waiting until their minimum retirement age, and then retiring with their full benefits.

Others however, are much more interested in retiring early and may or may not be willing to give up some of their benefits to make that happen.

Before we dig into the details of retiring early, we have to understand what a normal retirement might look like. To retire with an immediate and unreduced pension, one must meet one of the following:

Age 62 with at least 5 years of service

Age 60 with at least 20 years of service

Minimum Retirement Age with at least 30 years of service

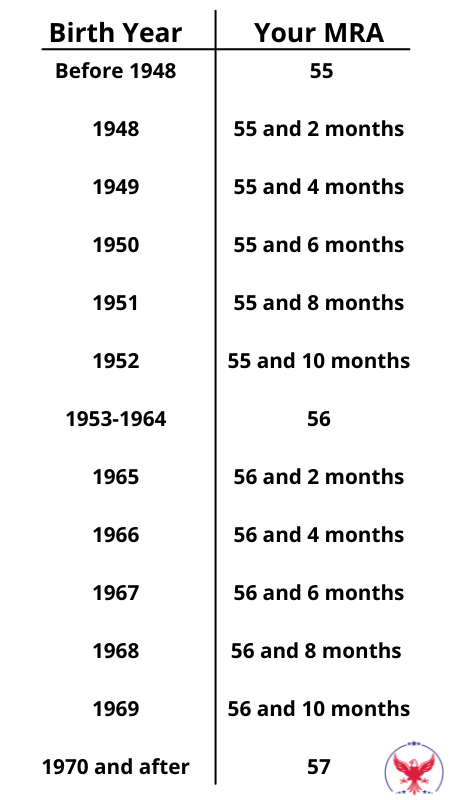

Your MRA (minimum retirement age) is based on your birthday per the chart below.

Note: The retirement rules for air traffic controllers, law enforcement officers, and firefighters are not the same as traditional FERS. See the section near the bottom of this article for the specifics on how this works for you.

FERS Postponed Vs. FERS Deferred Retirement

In the English language the words postponed and deferred have almost identical meanings but in the context of your federal benefits, these two types of retirements are very different from one another.

To help you understand the key differences we will go through the specifics as well as some examples of each type.

But just so you know upfront, one of the major differences between these types of retirement is your ability to continue your health insurance (FEHB) into retirement. For a postponed retirement you are able to turn your health insurance back on but with deferred retirement you are not.

Here is a chart of the key differences to understand:

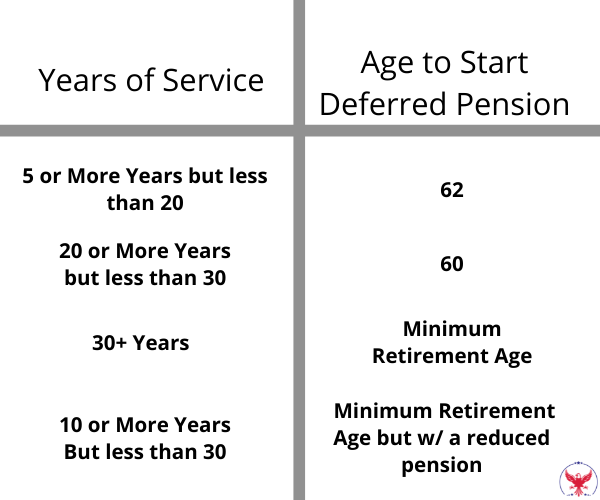

When Does My Deferred Retirement Pension Start?

So let’s say you have 5 years of service and you kept your contributions in the system, when can you start receiving your deferred pension?

It depends on how many years of service you have per the chart below.

As the chart shows, the more years of service you have, the sooner you’ll be able to turn on your deferred pension later.

For example, if you have 5 years of service the earliest you can start drawing a pension is age 62. But if you have 30 years of service then you can start your deferred pension at your minimum retirement age.