Gone are the days of MASSIVE CSRS pensions.

There are only a small percentage of CSRS (the old system) employees left in the government and their HUGE pensions are dying with them.

But FERS (the new system) federal employees still have good benefits if you know how to maximize them.

Instead of 1 HUGE pension, FERS have 3 retirement income sources that can be substantial if managed well.

Your 3-Legged Retirement

FERS federal employees’ core retirement income will come from these 3 sources:

FERS Pension/Annuity

Social Security (And Maybe the FERS Supplement if you Qualify)

TSP (Thrift Savings Plan)

But I have bad news. Just being a federal employee is not enough to ensure that these benefits are maximized.

But there are strategies that you can use to make sure you get the benefits that you deserve.

FERS Pension/Annuity

Note: Your FERS pension is sometimes called an ‘Annuity’ especially on official government documents. But most people call it a pension.

Your FERS Pension is a monthly payment that you’ll get as a federal retiree for the rest of your life. The amount you’ll receive from your pension depends on three factors:

Years of Creditable Service

The more years of service you have, the bigger your pension will be.

But not all government work is creditable for your retirement. For example, temporary* service that occurred after 1989 will not count towards your FERS retirement or your FERS pension.

However, if you were active duty military or a reservist that was activated, then that time can be “bought back” to make it count towards your FERS retirement and increase your pension. If you aren’t sure if you should buy back your military time then check out this full guide to make sure you maximize what you have.

*Temporary time is normally defined as federal service during which you were not paying into the retirement system from your paychecks.

How to Maximize Years of Creditable Service

Unused sick leave can count as creditable years of service to increase your pension. Here is a link to an article if you would like to know more about that.

A more obvious solution to getting more years of creditable service is just working longer. Some people love their jobs and are just fine working longer. Others can’t wait to leave and working longer just isn’t worth it.

High-3 Salary

Put simply, your high-3 is your highest average salary during your highest paid 36 consecutive months of your career.

For many people, their high-3 comes from the last 3 years of their career because that is when they got paid the most. That being said, it is important to know that it doesn’t have to be the last 3 years of your career. Your high-3 will automatically be the 3 years that you had the highest pay regardless of when it occurred in your career.

Note: Your high-3 does not have to be 3 calendar years (ie January-December). For example, if you had the highest average basic pay between May 2013 and May 2016 then that is the 3 years that will be used.

To maximize their high-3 salary, many Feds decide to apply for higher paying positions or move to a state with a high locality pay. Feds like to do either of these two things during their last 3 years of service when their salary is the highest.

Multiplier

Your multiplier will be 1% unless you retire at age 62 or older with at least 20 years of service, at which point your multiplier would be 1.1% (a 10% raise!).

This bump in pension is often the incentive that many feds need to work just a bit longer. Do the math for your own pension here to see what would happen if you worked until age 62 and 20 years of service.

Social Security

Like most retirees, federal employees can enjoy the benefits of social security. Social security is also a fixed income source that lasts until the death of the federal employee. Your social security benefit is calculated from your highest 35 earning years of work. The earliest you can receive social security is at age 62.

For example: you could retire from the federal government at age 62 and not receive social security benefits until age 70.If you would like to know when to start receiving social security benefits as a federal retiree, check out this article.

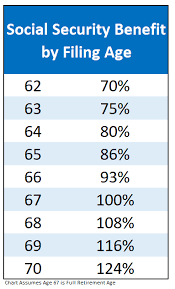

This chart shows how the social security benefit increases over time:

Maximizing your social security benefit has everything to do with timing. We can see that if you wait longer, your benefit will be greater. But, if you start at age 62, you receive benefits sooner. If everyone knew when they were going to die, this decision would be a lot easier. Feel free to check out this article about when to take social security.

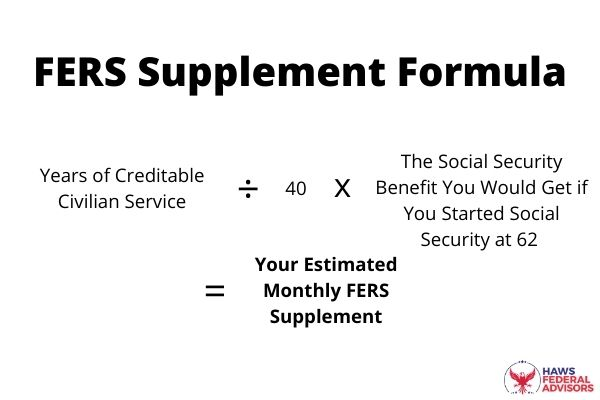

FERS Supplement

The FERS supplement is only available to certain federal employees. It is similar to the pension in that it is a fixed income source. But, unlike the FERS pension it is only available to federal employees who retire with a full retirement from ages 57 to 62. To receive it, you must have at least 30 years of service at your MRA (age 57 for most people) or have at least 20 years of service at age 60.

The FERS supplement is based on your years of service and your social security benefit at age 62. If you would like to know more information to see if you qualify for this benefit, feel free to check out this article.

Here is the FERS Supplement Formula:

Maximizing your years of service and social security benefits will allow you to get a bigger FERS supplement.

TSP

The TSP (Thrift Savings Plan) is a retirement plan for federal employees. It is similar to a 401k or IRA. The TSP gives federal employees the opportunity to save and invest in 5 different funds (C,S, I, G, & F) throughout their career. By the time a federal employee retires, their TSP fund can have hundreds of thousands or millions of dollars.

With their TSP money, federal employees are able to create another potential source of income in retirement. But, unlike the fixed income sources we’ve discussed thus far, the TSP can be much more flexible.

While you’re working, there’s a few things you can do to maximize your TSP. The first one would be to save more money. Second would be knowing what funds to invest in depending on where you are in your career. And lastly would be taking advantage of the traditional and Roth TSP. If you would like to see how to implement these steps, check out this article.

Conclusion

Transitioning from your career to retirement can be a stressful time and a difficult transition.

But knowing that you’ll have plenty of retirement income in retirement makes the transition much easier.

If you would like to have a one-on-one meeting with us to discuss your personal financial situation, feel free to schedule an appointment here.