How Much Does it Cost to Buy Back Military Time?

But just like most good things in life, there is a cost. And the cost will be based on your military base pay and when you served. The chart below shows the percentage of your basic pay that you’d have to pay to buy back your time during different years.

Source: https://www.opm.gov/retirement-services/fers-information/service-credit/#military

For most years, it will be 3% for FERS employees.

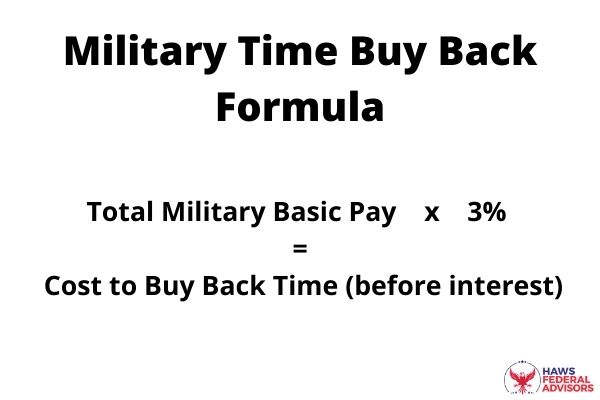

Here is the formula to calculate your military deposit (aka, what it costs to buy back your military time).

Total Military Basic Pay x 3%* = Cost to Buy Back Time (before interest)

*This will be higher than 3% for time between 1999-2000. See chart above.

So basically you need to add up every year’s basic pay and multiply that by 3%.

Here’s an example.

Let’s say you had 6 years of service back in the early 90’s and had the following basic pay during those years:

1990: $13,000

1991: $14,000

1992: $16,000

1993: $18,000

1994: $20,000

1995: $21,000

Total Basic Pay: $102,000

Note: Your Basic pay does not include allowances, flight pay, combat pay, etc.

This means that it would cost the following to buy back these 6 years before we think about interest:

$102,000 x 3% = $3,060 (before interest)

But Wait, There’s More!

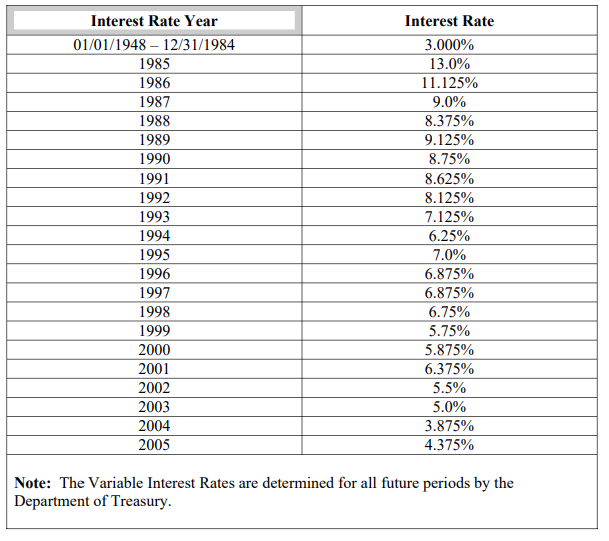

But we are not out of the woods yet. Most federal employees will also have to pay interest on their deposit as well. The interest rate is different every year but as you can imagine, the longer you wait to buy back your military time, the more it is going to cost you.

Here is a chart showing the interest rate from previous years.

Source: https://www.opm.gov/forms/pdf_fill/opm1514.pdf

But with current interest rates being much lower than they were in the past, the variable interest rate for military deposits have been much lower in recent years. In 2021, it is 1.375%.

So basically, for every year (after the grace period which we’ll discuss below) that you work at your civilian job, the amount that you would owe, if you choose to buy back your military time, would increase per the amount of interest due that year.

And while the interest calculation can get a little hairy, the most important thing is that you buy back your time as soon as possible so as to not accrue more interest.