We all have heard the common regret of “I wish I would have started investing earlier”. Or “If only I knew then what I know now”. But unfortunately, there is nothing we can do to change the past. Fortunately, we can learn from our own past as well as the past of others to make our future bright despite our mistakes.

And because we all hear the regretful almost-retiree talking about starting earlier, I figured it could be helpful for all of us to see an example of why investing early and consistently makes such a difference. Or in other words, why it pays to be the tortoise instead of the hare in the race of an incredible retirement and a robust TSP.

In this example, our tortoise fed is named Julie and our hare fed is name Robert. They both start their careers at 27 and both make $75,000/year. We’ll assume that their salary stays the same for their entire career to keep the numbers easy. Julie, right out of the gate, decides to invest 10% of her salary into the TSP. She got used to living on the lower amount and never thought much about it. Robert, on the other hand, decides that he is very far from retirement and will opt out of the TSP for now.

Now let’s fast forward 10 years. Both Julie and Robert are 37 and they both think about their TSP again. Julie realizes that she has already accumulated $169,781 (we’ll assume a 8% return for this entire example) and is pleasantly surprised. Robert talks to Julie and realizes that he really needs to start using his TSP. He decides to take a pretty drastic cut to his lifestyle to start contributing 10% of his salary into the TSP as well.

Fast forward 10 years again. They are both 47 and Julie now has $536,325 in her TSP and Robert has $169,781. They talk again and Robert gets fiercely competitive. He wants to contribute more than Julie so he takes another drastic cut to his lifestyle and starts contributing 20% of his salary into his TSP. Julie decides to stick to her 10%.

Fast forward 10 years one last time. They are both 57 and Julie is ready to retire. She has accumulated a whopping $1,327,666 in her TSP and she has plenty to cover the gap between now and when she starts drawing social security at 70 so that she can get higher social security payments. She is confident in her retirement and her financial freedom. She buys a vacation home and lives a comfortable life.

Robert has done pretty well too. He has accumulated $649,643 in his TSP but decides to work a few extra years because he doesn’t want to eat through a major portion of his TSP trying to fill the gap before he starts social security. He too has a good retirement but definitely doesn’t have the same cushion and freedom that Julie now enjoys.

In the end, Julie ended up with more than twice the amount of retirement savings than Robert but this is not very surprising by itself. The surprising part shows up when we look at how much they each put into the TSP themselves. This charts makes it a little easier to see:

Both Julie and Robert contributed the same amount to their TSP accounts during their careers but when they contributed it made all the difference in the world. Julie was consistent the whole time while Robert had a late start and rushed to catch up near the end.

And while the details and amounts are different, I have seen this same story play out over and over again in real life. There are those feds that start early and stay consistent and are pleasantly surprised how much they end up with. And there are those that rush to catch up near the end. And as we have seen, the results tend to be dramatically different between the two groups.

But I don’t write this to discourage those that might have had a late start. We all have things that we wish we could go back and change. All we have is now and there is still so much we can do to prepare for the future.

If you want help knowing what you need to do to be best prepared for retirement, it may make sense to talk to a professional that understands your needs and federal benefits. But regardless of where we are at or what we have already done, we can all do something today to make your future that much brighter.

When you are young and early in your career, it often makes sense to put the majority of your TSP in the C, S, and I funds. And because young feds tend to have a lot of time before retirement, they don’t mind that these funds bounce around because overtime, they grow at a fast rate.

But as you progress through your career and approach retirement, it often makes sense to introduce more of the F and G fund. These funds won’t grow nearly as fast, but they will provide more of the stability you need in retirement.

But even in retirement, I almost never recommend going 100% into the G fund. The G fund is safe but won’t grow enough to beat inflation and maintain your lifestyle over time.

Having a good mixture of funds allows the more stable funds (G and F) to provide consistent cash for your retirement lifestyle and the other funds (C, S, and I) to beat inflation and continue to grow your wealth.

At this point, some of you might have noticed that I haven’t mentioned the L funds. And this is because the L funds are not independent funds. They are just a mixture of the other 5 funds.

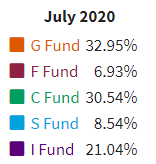

For example, this is the allocation of the L 2030 fund as of July 2020:

Source: https://www.tsp.gov/funds-lifecycle/l-2030/

What makes the L funds useful is that the allocation will automatically become more conservative (transfer more to the F and G funds) as time goes on. The purpose of these funds are so that employees can “set it and forget it”. In practice, feds pick the L fund that is closest to their retirement date and they don’t have to think about it again.

My problem with the L funds is that this approach doesn’t make sense for everyone. For example, I have a client who is close to retirement. Once he retires, his social security and pension income will be more than enough to pay for his expenses so he is not planning on using his TSP balance for some time. In his case, we are able to invest his TSP more aggressively because he has a substantial amount of time before he needs the money. If he had chosen an L fund, the allocation would have been far too conservative for him.

The L funds are not bad funds but you have to make sure it makes sense for you before investing in them.

Always keep in mind that there is no perfect TSP allocation. It all depends on your situation and goals. The exact percentage of each fund that makes sense for you will often be different than what makes sense for your co-workers.

The best thing to do is to educate yourself enough to make an informed decision. A financial advisor who understands the TSP can be a huge asset in this process as well. Because regardless of where you are in your career, getting your TSP right can make a huge difference over your career and retirement.

Once you come up with a TSP allocation plan that makes sense for you, stick to your plan. Don’t worry about what the market is doing. Focus on what you can control and not on what you can’t.

You can’t control the markets but you can control how much you set aside for retirement. You can’t control the economy but you can control how well you plan for the future. The good news is that by reading this book and educating yourself, you took one more step towards being prepared for whatever comes your way.