For any federal employee who is looking to get serious about planning for retirement it is critical to contribute and invest in retirement accounts.

Most federal employees are taking advantage of the TSP but many are now thinking about an IRA as well.

Note: To learn more about how IRAs compare to your TSP, check out this article.

And one question that then arises is if there is anything stopping federal employees from using both their TSP and IRAs at the same time to put their retirement savings into overdrive?

Put simply, sometimes you can and sometimes you can’t depending on your income and situation.

This article will help you understand if you can use both the TSP and an IRA to be better prepared for retirement.

The TSP’s For Everyone

The first thing I want to mention is that no matter your income or situation, you are always allowed to use your TSP as a federal employee. So even if the rest of this article shows you that you can’t use an IRA how you’d like then you will always have your TSP to prepare for retirement.

When You Can and Can’t Use a Traditional IRA

The rules for using a Roth and traditional IRA are different so I will start with the traditional IRA side.

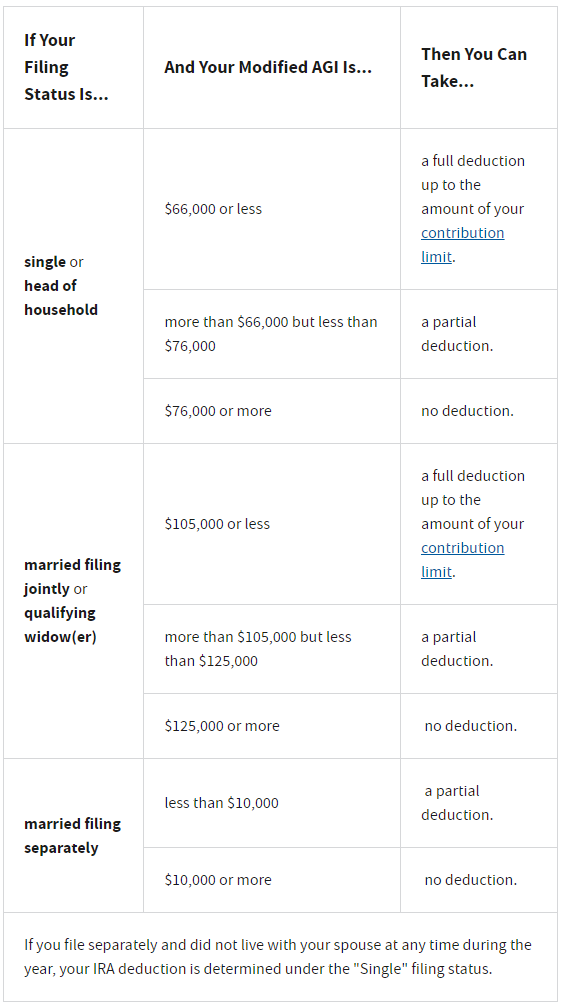

You are always allowed to contribute into a traditional IRA as long as you are working. However, you may not be able to deduct your contributions (aka lower your taxes) once your income passes certain thresholds.

The thresholds are shown here with this chart.

Note: This chart only applies to your traditional IRA contributions as a federal employee covered by the TSP as well. The rules are slightly different for a spouse who is working but not covered under a plan at work which I’ll discuss below. If neither spouse is covered at work then they will always be able to deduct traditional IRA contributions regardless of income.

Source: IRS.Gov

So basically, as your income increases, your ability to deduct your traditional IRA contributions goes away.

For spouses of federal employees who are working but not covered under a retirement plan at work, the following chart applies to determine if you can deduct your IRA contributions.

Source: IRS.Gov

When You Can and Can’t Use a Roth IRA

The good news is that the rules for when you can and can’t use a Roth IRA are a lot simpler than the rules for a traditional IRA.

For a Roth IRA it all comes down to what your income is and has nothing to do with whether you or your spouse are covered under a plan at work.

However, once your income passes certain limits then you can’t put money directly into a Roth IRA at all.

This chart shows how it breaks down for your tax filing status.

Source: IRS.Gov

So as an example, if you file married filing jointly and have a modified adjusted gross income of more than $208,000 then neither you or your spouse can put money directly into a Roth IRA at all.