This article’s topic is so important when it comes to planning for retirement. If you understand it then you will have much fewer surprises down the road.

A huge misconception that I see all the time is about taxes in retirement and specifically, on your pension. Many people believe that after putting in 20 or 30 years (and paying taxes the whole way) the tax rules will lighten up in retirement. In some ways they do but in many ways they don’t.

Taxes on Your FERS Pension

During your career you do pay a portion of your paycheck into the FERS retirement system (the system that funds your pension). And that money that you paid in you actually does come out tax free because you already pay taxes on it. Unfortunately, it’s only a very small percentage of your pension.

First, they add up everything you paid into the system and then they spread that over your projected retirement. For example, let’s say you paid $30,000 in the system during your career. If the government projected you to have a 30 year retirement, that would mean that $1,000 dollars of your pension would not be taxable each year. So, in most cases, about 95% to 98% of your pension is taxable.

While I am not going to focus on it during this article, I do want to mention that the majority of Social Security (for most federal employees) is taxable as well. Because of this, many feds are surprised by how high their tax bracket is in retirement.

In many cases, the following happens.

Someone calculates that their gross pension will be $3,000/month and they are happy with that because that is about one of their paychecks. They retire and then realize that after taxes and reductions, their pension is not as big as they thought it would be. Because of this they need to pull more money out of their TSP to fill the gap.

When they do pull money out of their TSP they remember that that is taxable as well. Instead of taking out just enough to fill their gap, they’ll have to take our more to be left with the amount they need after taxes. Overall, they end up using much more of their retirement savings than they had initially thought.

More Reductions

The key is knowing exactly what spendable income (after reductions and taxes) you are going to have in retirement. This allows you to go into retirement with your eye wide open.

As I mentioned earlier, taxes are not the only thing that comes out of your pension before you see it. There are also a number of other reductions that may include:

-Survivor Benefits

-Taxes

-FEHB Premiums

-Penalties for retiring with an early retirement (MRA+10)

-Other premiums (ie FEGLI, Vision and Dental, ect.)

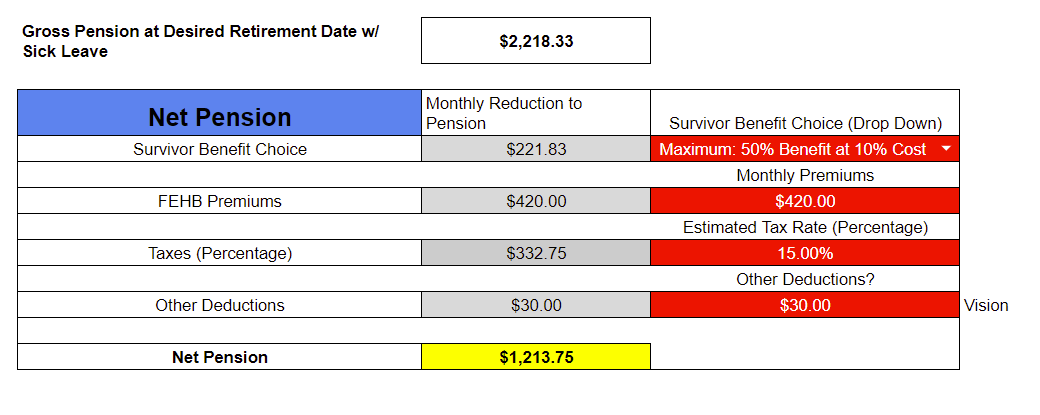

And to show you what this might look like, here is an example:

In this example, the person started out with a monthly gross pension of $2,218 but after some very typical reductions, they will only have about $1,213 of spendable income every month.

I am not going to dig into each reduction (I have done this in other articles) but I share this because it is often very eye-opening to see what your pension might actually be.

And unfortunately, there is no perfect way to completely eliminate reductions and taxes in retirement so for most people, the best strategy is being thoroughly prepared beforehand. The worst case scenario is being blindsided in retirement. Retirement can be a great time especially if you go into it with your eyes wide open fully confident that you are in a great financial position.