Table of Contents

What is The Difference Between The Traditional TSP and Roth TSP?

-How Does The Traditional TSP Work?

-How To Make Sure Your Roth TSP Comes Out Tax Free

Other Major Differences/Considerations Between Traditional and Roth TSP

-When You Can Access The Accounts

-Your Traditional TSP Will Affect Other Things

-How Much Money You Need At Once

-Required Minimum Distributions (RMDs)

So Which is Better, Traditional or Roth TSP?

-When The Traditional TSP is Better

-When You Should Have Both: Tax Diversification

-Do my agency matching contributions go into my traditional TSP?

-Do I get matching contributions if I only use the Roth TSP?

-Can I contribute to the Roth TSP and traditional TSP at the same time?

-How much money can I put in my TSP between the traditional and Roth?

-Can I convert my traditional TSP to the Roth TSP?

When The Traditional TSP is Better

The traditional TSP is a great way to keep your taxes during your career especially if you are a high earner.

And because you lower your AGI (adjusted gross income) by using the traditional TSP it may also keep you within the threshold to qualify for certain tax credits and perks like Child Tax Credits and IRA Contribution Limits.

It can be especially helpful for those that are nearing the end of their career because their income is probably as high as it will ever be.

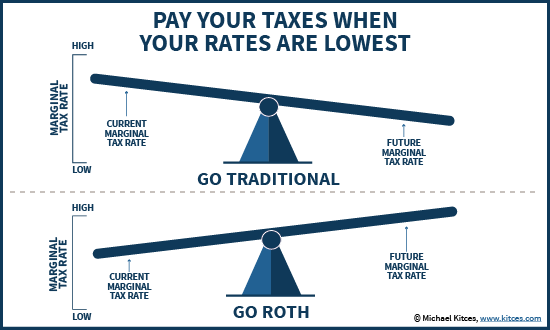

Source: Kitces.com