If you have watched my content for some time then I am sure that you know how helpful a Roth TSP(Thrift Savings Plan) or Roth IRA account can be in retirement.

After all, these accounts can help save a tremendous amount in taxes over the course of your career and retirement.

But what is the best way to get money into these accounts?

For some, it may seem like the simplest way to get money into the Roth TSP would be to simply move some of their existing traditional TSP balance over to the Roth side.

Unfortunately, it isn’t that simple.

Wait.. HOLD UP!

Is Roth really the best option for you?

If you aren’t sure, you are going to want to check out this article that compares whether you should be using the Traditional TSP or Roth TSP

Sorry, Can’t Do That

The first thing to know about getting money into the Roth TSP is that the TSP doesn’t allow you to move money from an existing traditional TSP to a Roth TSP.

P.S: If you aren’t familiar with all the cool benefits of a Roth account, check out this article.

So the only way for most people to get money into the Roth TSP is by contributing straight into it from your paycheck.

For example, if you have 50k in your traditional TSP you can’t move that into your Roth TSP but you can start putting new money directly into the Roth TSP. And this is done the same way that you put money into the traditional TSP.

You simply let the TSP know (usually through your account online) that you now would like to put a piece of paycheck into the Roth TSP instead of (or in addition to) what you are putting into the traditional TSP.

Note: The only other way to get money into your Roth TSP account (outside of contributing money from your paycheck) is by moving another Roth employer plan into it like a Roth 401k or Roth 403b.

But please know that the TSP does not currently accept transfers from Roth IRAs.

But There’s Another Way

Now with all that being said, there is another way to get your traditional TSP money into a Roth account to benefit from the tax advantages.

This is done by using a Roth IRA.

To learn more about the TSP Vs. IRA check out this ultimate guide.

But just know, the strategy that I am about to talk about only works for those that are at least 59 and ½ or have already left federal service.

Once you are at least 59 and ½ or have left federal service you would be able to move your TSP money over to a Roth IRA. But I wouldn’t recommend going straight from the TSP to a Roth IRA.

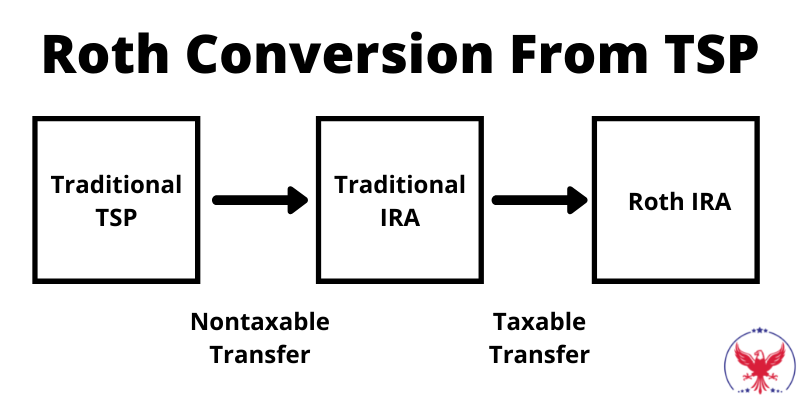

The best way (in my experience) to make the transfer is by first moving your money to a traditional IRA and then over to a Roth IRA.

This process is shown in the picture below.

As the chart shows, when you move money from the traditional TSP to Traditional IRA no taxes are due no matter how much you transfer.

However, anything you then move to a Roth IRA would be taxable so you probably want to limit how much you convert every tax year.

When Should You Move Money to a Roth IRA?

There are a number of occasions when it makes sense to move money over to a Roth IRA but here are a few.

Higher Taxes In Future

Whenever you predict that you will be in a higher tax bracket in the future then it may be worth moving money to a Roth IRA which means you’ll pay taxes at today’s lower tax rates and avoid taxes in the future.

Down Market

Whenever the market goes down in value then so will some of your investments and this is often a great time to move money to a Roth IRA.

When your investments lose value then that means that you will have to pay less dollars in taxes to move that money over to a Roth IRA. And when the market later recovers then your now larger Roth IRA will be able to grow along with it.

For example, let’s say your traditional IRA balance is $10 in year one, $5 in year two, and $10 in year three and let’s assume that the decrease in value that we saw in year two is because the market lost value.

Well if we had to pick one of those years to do a Roth conversion then which one would you pick? Definitely year two because we would only have to pay taxes on $5 instead of $10 and then in year three your $5 would now grow back up to $10 in a Roth IRA.

But… Be Careful!

Getting money to a Roth IRA has a ton of benefits but there are some major pitfalls you will want to avoid.

One of the biggest things to know is the 5-year rule.

This is the rule in a nutshell: If you are under 59 and ½ then you have to wait 5 years after each conversion before you can pull the money out of your Roth IRA without any penalties.

So if you are over 59 and ½ then you don’t have to worry about this 5-year rule.

If you are under 59 and ½ then here is an example of how it would work:

Example

Let’s say you are 50 years old and move $10,000 from your traditional IRA to your Roth IRA. For you to withdraw that $10,000 from your Roth IRA without any penalties you would have to wait 5 years which would be the year you turn 55 in this example.

This article goes into depth on how this rule works.

Final Thoughts

Just like anything in life, the best decision depends a lot on your personal situation.

This is no different. You will want to make sure that a Roth IRA and Roth conversions make sense for you before moving forward.

Common Questions

Can my agency’s matching contributions go into my Roth TSP?

As of right now (2023) agency matching contributions always go to your traditional TSP.

However, in late 2022 a new law was passed that would allow agency contributions to go into the Roth TSP as well. We are just waiting for this to be implemented.

How do loans/withdrawals affect your Roth and traditional balances?

Loans will pull the money proportional between both your traditional and Roth TSP accounts.

For example, if 80% of your money is traditional and the last 20% is Roth then 80% of the loan amount will come from the traditional side and 20% from the Roth.

For withdrawals, you can pick which account you’d like to pull from or you can also do proportional.

Are Roth Conversions the Same as a Backdoor Roth?

No, these are two separate things.

A backdoor Roth is done while working because someone makes too much money to contribute into a Roth IRA directly.

A Roth conversion is what this article is about. It is moving money from a traditional (pre-tax) account to a Roth account normally in retirement.

Do I get the 10% penalty if I move money to a Roth IRA before 59 and ½ ?

No, doing a Roth conversion to get money to a Roth IRA before 59 and ½ will not spark a 10% early withdrawal penalty.

But sending money to your personal checking/savings account from your retirement accounts before 59 and ½ can spark the 10% penalty.