FEGLI (your federal life insurance) has major extremes in retirement.

It can be your saving grace or just crazy expensive and not worth it at all.

It all comes down to what parts of FEGLI you choose to take with you into retirement.

Background

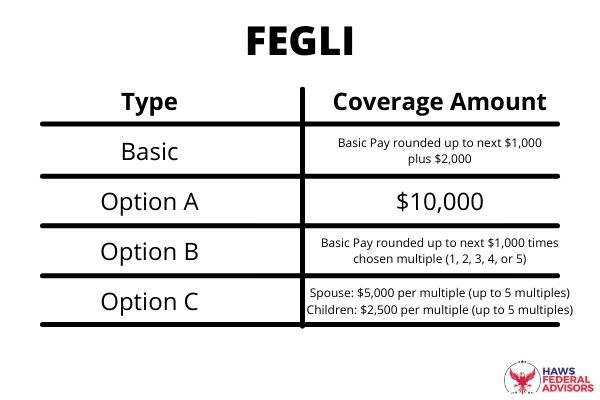

FEGLI has 4 different parts and they all work a little differently at retirement.

Here is a chart that summarizes the 4 parts:

When people complain about how expensive their FEGLI is they are normally talking about FEGLI option B as that one gets expensive as you age.

First Step: The first thing to check is exactly what parts of FEGLI you have!

Popular Answer

Most people do one of these two things with their FEGLI at retirement:

Get rid of their FEGLI completely as they don’t need life insurance any more at that point

Get rid of Part B and C but take FEGLI basic (75% Reduction) and Part A as both of these options become free after age 65 (I’ll explain the details of how this works lower down).

But What If I Need More?

If you know you need more life insurance in retirement than just FEGLI Basic (75% reduction) and option A then you’ll want to understand more of the details of how the other parts work in retirement.

You also may want to see if you can get a private life insurance policy at a cheaper rate.

Basic Coverage into Retirement

When you retire you have a few options when it comes to how much of your Basic Coverage you keep after the age of 65. There is a 75% reduction, 50% reduction, or no reduction option.

And of course you can completely cancel your Basic coverage in retirement if you want as well.

If you elect the 75 Percent Reduction, when you turn 65 or retire (whichever is later), your Basic insurance coverage reduces by 2 percent each month until the amount has been reduced by 75 percent. When the reduction is complete, the remaining 25 percent of coverage will continue for the rest of your life.

If you elect the 75 percent reduction then the coverage will become free at 65 or when you retire if that is later than 65.

If you elect the 50% reduction or the no reduction options then there will be a premium that you will have to pay for as long as you want coverage.

Basic 75% Reduction Example

Since this is one of the most popular elections, let me show what 75% reduction actually looks like.

Let’s say your salary is 100k and you are paying about $35/month for FEGLI basic while working.

Note: Your FEGLI Basic coverage amount is based on your salary so while working your beneficiary would get about 100k from your Basic FEGLI if you died.

If you retire at 57 and elect the 75% reduction option then you’d continue to have 100k-ish worth of coverage and would continue to pay $35/month.

This all stays the same until you turn 65 at which point your premiums ($35/month) goes away and you never have to pay for it again.

However, your coverage amount (100k) starts to go down a little bit every month until it reaches 25% of what it was before.

So in this example, 100k of coverage would be reduced down to 25k worth of coverage after 65.

If you retire at 65 or later and elect 75% reduction then the premiums would go away right at retirement and your coverage amount would immediately start reducing down to 25% of what it was before.

Option A into Retirement

If you carry Option A into retirement it acts similar to Basic coverage but there are no elections to be made. Your Option A coverage will automatically decrease by 2% per month until it has reached a 75% reduction ($2,500 left) at the age of 65 or retirement if that is later. This coverage becomes free at that point as well.

Option B and C into Retirement

With Options B and C you will have elections to make if you choose to continue them into retirement. You will have to decide how many multiples of each you’d like to keep in retirement.

You will also have to decide if you’d like a full reduction at age 65 (or retirement if later) or no reduction.

If you select a full reduction then your coverage (starting at age 65 or retirement if later) will decrease by 2% each month until it has been reduced by 100%. But picking the full reduction option does mean that the coverage does become free once the 2% reduction begins.

The downside of selecting the no reduction option is that it becomes very expensive to keep as you age.

If you want to see what it would cost for you to keep different options into retirement then check out this FEGLI Calculator.

Example

Here is an example to show you how expensive FEGLI can be if you want to keep it 100% throughout retirement.

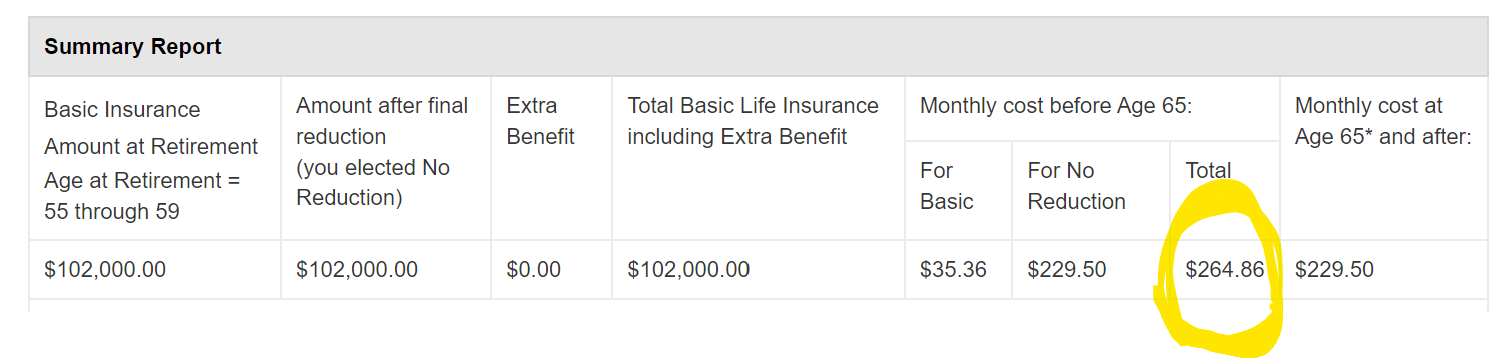

Again, let’s say your salary is about 100k and you retire at 57.

If you wanted to keep Full FEGLI Basic (not the 75% reduction options) the cost would change for $35/month to $265/month!!

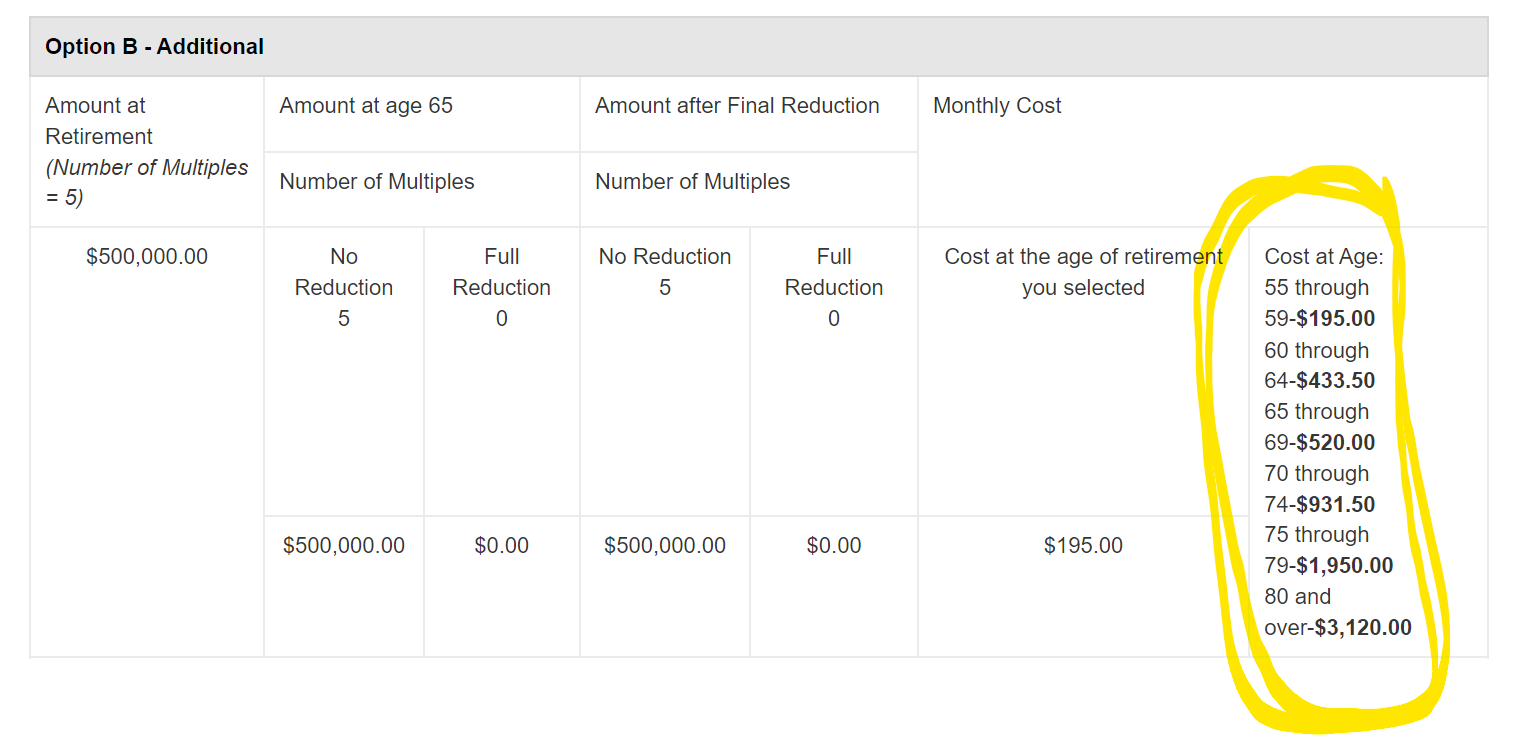

Now if you had FEGLI part B at 5x your salary then trying to keep that at 100% into retirement would be even more extreme.

The price would start at $195/month but would almost double every 5 years as shown in the chart below.

Final Thoughts

FEGLI can be a helpful benefit if you know how it works and when it makes sense to get out.

Most people don’t have have life insurance needs deep into retirement but it is up to you to decide what options make sense for your budget and your loved ones.