If you are over 50 and still have FEGLI you are losing money!

Unless of course FEGLI is your only option.

For most people, FEGLI prices get out of control as you approach retirement.

But there are things you can do about it.

What Part Again?

Not all parts of FEGLI increase their prices with your age.

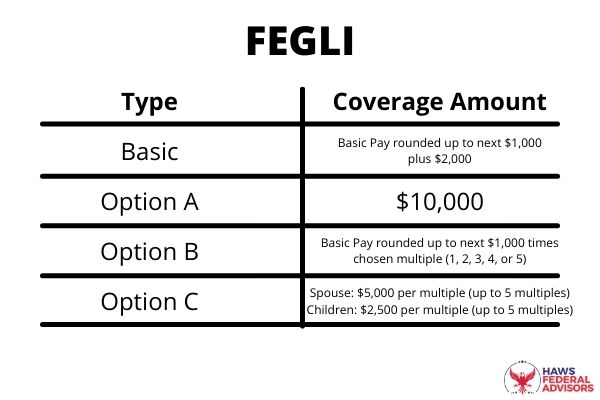

There are 4 parts of FEGLI and this picture summarizes what they cover:

The pricing for FEGLI Basic is the same for all employees regardless of age.

The pricing for FEGLI parts A, B, and C do go up with age but Option A and C are never that expensive as they don’t cover much.

Option B however can get very expensive as you can get up to 5x your salary worth of coverage.

Nutshell: FEGLI part B is often the troublemaker as the pricing goes up as you age especially if you have a high multiple of your salary in coverage.

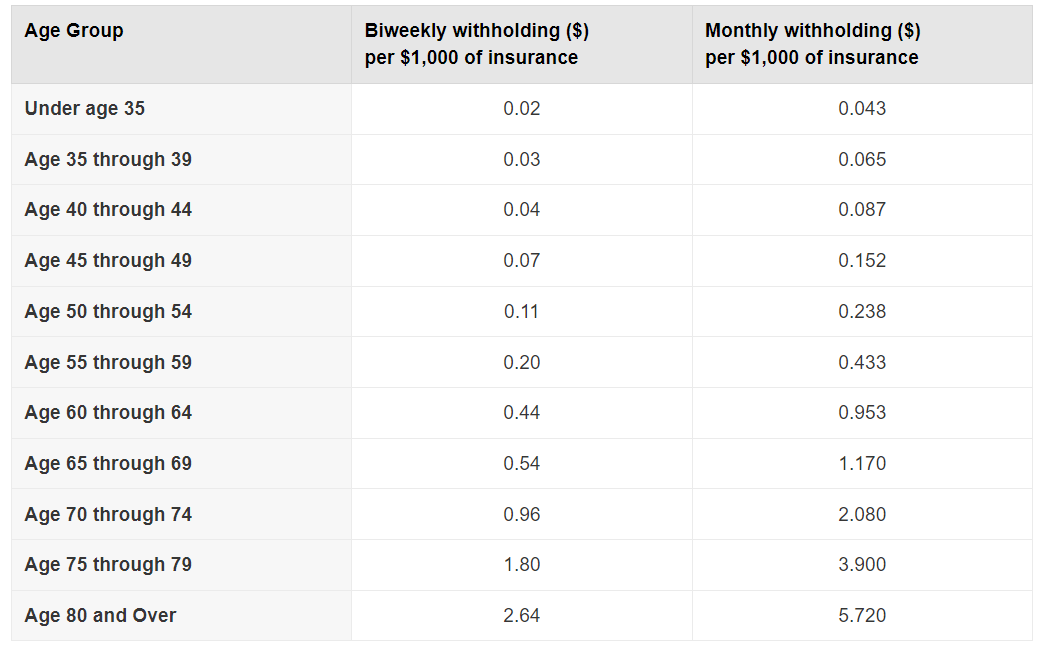

How Bad Does it Get?

This chart shows how the pricing works for part B as you age:

Source: OPM

The pricing is pretty reasonable until you are 50+ at which point the pricing almost doubles every 5 years!!!

So if you are 54 years old and paying $100/paycheck right now then once you hit age 55 then you’ll pay almost $200/paycheck for the same coverage.

Better Options

There are three things that federal employees do once they learn how expensive FEGLI part B can be.

1. They cut/reduce their FEGLI

a. People do this if they realize they simply don’t need life insurance any more. Maybe their kids are grown and their big debts are paid off.

2. They replace their FEGLI

a. If you are in decent health then you can probably replace FEGLI with a cheaper policy in the private sector. Most go get the cheapest term policy they can find that will last however long they need coverage for. But most private sector policies will require a medical exam to get coverage so you won’t qualify if you have serious health conditions.

3. They keep their FEGLI

a. If you have poor health then you may not qualify for cheaper insurance in the private sector. So if you still need life insurance but have poor health then keeping FEGLI may be the best option for you. FEGLI may be expensive but it is still the best option for some.

But I’m Still Young

If you are still young and the FEGLI part B is still reasonably priced then you can stay on FEGLI for a while but many young people still move to a well-priced term policy from the private sector so they can lock in a price for a chosen amount of time.

Final Thoughts

For some, FEGLI part B is the best option while others can save thousands of dollars by switching to a private policy.

It is up to you to shop around to see what is the most effective way to protect you and your family.