The TSP is an emotional thing. It is an essential retirement planning tool and no one wants to run out of money in retirement.

This is why it is so important to have a strategy that allows you to almost never lose money in the TSP.

Here are 2 strategies that will help you do just that (but I only recommend one of them).

Too Risky for Me

As some people start investing and become exposed to the risks that are involved some people decide that it is simply not for them. These people typically just save money in a savings account or the G fund where they know they can’t lose money.

The problem with this strategy is that just like there are risks that come with investing there are also risks that come from not investing (not to mention the missed tax advantages if you don’t save in a retirement account).

Because the U.S has a long term inflation rate of close to 3%, someone is almost guaranteed to lose purchasing power if they don’t earn at least that overtime. The actual dollar amount that they have in their accounts may not go down but the amount of money that it takes to purchase everyday items will certainly go up overtime.

Investing too conservatively can be just as devastating to retirement savings as being too aggressive.

A Better Strategy

If you are a homeowner, has your home ever gone down significantly in value? If so, by how much? If you are like most homeowners, it is hard to know exactly.

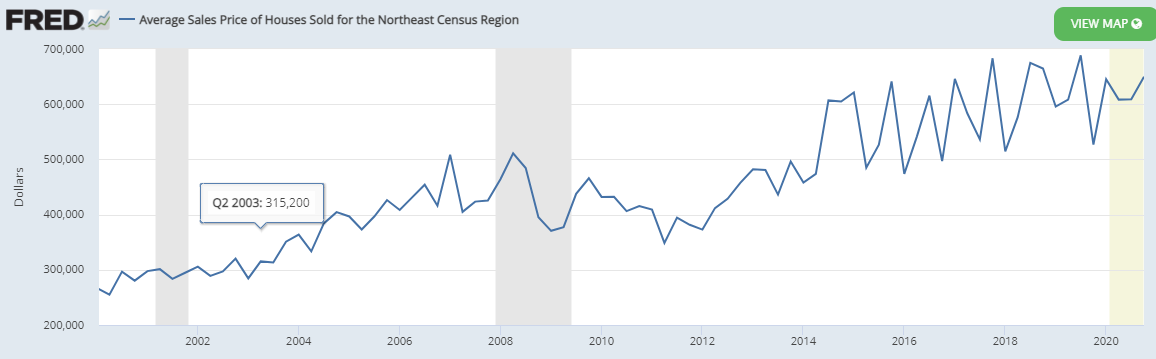

Some people believe that real estate almost never loses value. But if we look at the data, this is simply not the case. The below graph shows the median sales price for homes in the northeast over the last 20 years.

Source: https://fred.stlouisfed.org

As we can see, home values fluctuated by more than 100k many times in the last 20 years.

Then why do some believe that real estate almost never loses value? In my opinion, it is because it is so much harder to find out what your home is actually worth.

If you want to see where your TSP account balance is at, you simply log in. If you want to know what your home is worth, you have to get an appraisal or put your house on the market.

Consequently, people check their home value far less often than they check their investments and if you only check every 10 years, the odds of your home being worth more now is very high (despite the many fluctuations in between).

Back To Your TSP

With our houses, we tend to naturally understand that we probably don’t want to sell our home when it is worth less than what we bought it for. We’d much prefer to sell when the market is hot and home values are up.

This way we’d almost never lose money.

This is the same approach that we should take with our retirement savings. It is important to remember that one of the only ways to lose money while investing is to sell when the market is down. If the market drops and we don’t sell (or move to the G fund) then we haven’t lost anything yet.

We only lock in our gains or losses when we sell.

The markets have always fluctuated and will continue to do so especially in the short term. But we have to remember that we are playing the long game. Short term fluctuations don’t matter much when we have a long term strategy.

What About in Retirement?

During one’s career, not selling retirement investments is relatively easy because we know that we don’t need the money for some time.

But what about in retirement when we have to sell some of our investments to live?

This is when a good strategy can make all the difference. One good way to help mitigate this problem is by having a cash bucket of 3-5 years of expenses (after fixed income like your pension and Social Security) invested in cash or near cash investments. The G fund may be a good fit for a portion of this money.

This allows you to continue to invest a portion of your TSP in stock based funds (to get the growth that you need over time) while having the flexibility of not having to sell these funds when the market is down because you have a cash bucket to pull from.

Conclusion

Watching your TSP go up and down can be a difficult thing to do especially as you approach retirement. But it is important to keep a long term perspective to make good decisions now and in the future.