Basic

When you first start with the federal government you will be automatically enrolled into basic coverage unless you choose to waive it.

Your basic coverage is equal to your annual basic pay rounded up to the nearest $1,000 plus $2,000.

For example, if your basic pay was $97,200 then to calculate your basic coverage amount you would round your pay up to $98,000 and then add $2,000 which would come to a total of $100,000 of coverage.

This basic coverage is the only part of FEGLI that the government helps pay for. For most employees the government pays ⅓ of the premiums and the employee picks up the other ⅔. But if you are a postal employee then The USPS pays 100% of your basic insurance premiums.

Extra Benefits for Basic Coverage

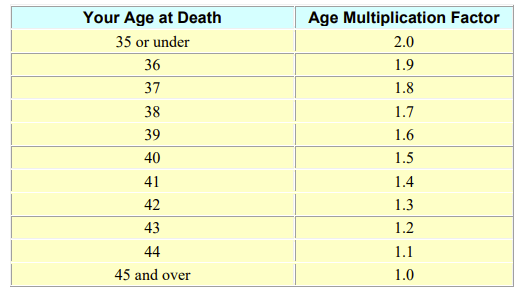

One added benefit of the basic coverage is the extra coverage that you get (for no extra cost) if you are under the age of 45.

If you are 35 or younger than you have 2x the normal basic coverage and this amount slowly goes down to only 1x between age 35 and 45. Once you are 45 or older than you will only have your normal coverage amount.

This chart shows how it decreases over time.

Source: https://www.opm.gov/healthcare-insurance/life-insurance/reference-materials/publications-forms/feglihandbook.pdf

For example, if your basic pay was $97,100 then your normal coverage amount would be $100,000. But if you are age 40 then you would have $150,000 of coverage.

This extra benefit applies only to basic coverage and not to option A, B, or C.

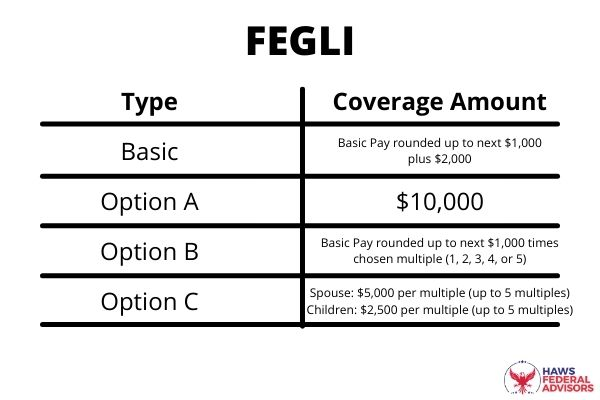

Here is a chart that summarizes the 4 different coverages.

How Much Does FEGLI Cost?

The cost of FEGLI will vary based on your age and, whether or not you are retired yet, and what FEGLI options you choose to take with you into retirement.

You can find the current FEGLI rates here.

For those that have substantial life insurance needs, part B is often used. And for those under 45, the rates tend to be very competitive for part B.

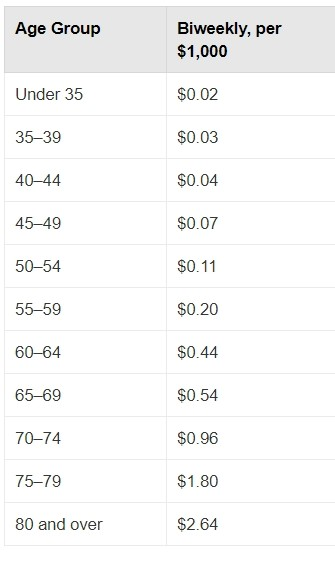

But as you get into your 50’s and 60’s, the cost of FEGLI part B starts to increase dramatically. As you can see on the chart below, the premiums skyrocket between ages 45 and 70.

For those who need life insurance and are in good health, it may be more cost effective to find coverage somewhere else as you age. But again, it can be difficult to get back into the FEGLI later so I would be very confident in your decision before you cancel any FEGLI coverage.

The Basic FEGLI coverage, on the other hand, is the coverage that you get automatically as an employee and the government pays for a portion of the premiums. The premiums for this coverage does not increase with age like it does for the other types. Consequently, some employees choose to keep this coverage for much longer than they keep the Option B coverage.

Basic Coverage Premiums per Thousand Dollar of Coverage (as of 2021) for Active Employees

Accidental Death and Dismemberment Coverage

This Accidental Death and Dismemberment coverage or AD&D is an extra (and automatic) part of Basic coverage and Option A coverage. Having Option B or C coverage will not increase the amount of AD&D coverage that you have.

If the event is eligible for AD&D coverage then these benefits will be paid out in addition to the other benefits that you may have.

For example, if you have Basic coverage and option B then (assuming the event is eligible for AD&D) then you would be able to get a payment from all three.

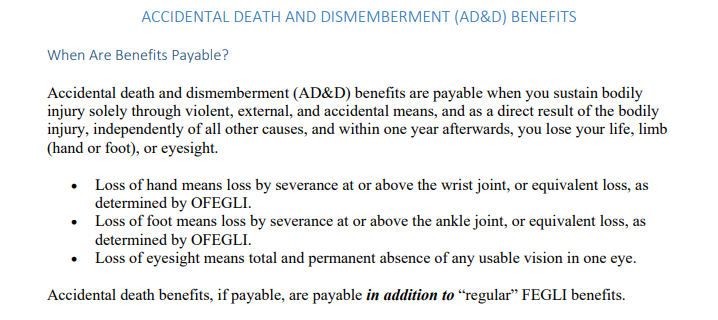

This is how OPM defines an event that is eligible for these benefits.

Source: https://www.opm.gov/healthcare-insurance/life-insurance/reference-materials/publications-forms/feglihandbook.pdf

If you pass away (or lose two limbs) from an event that is eligible then AD&D will pay out your Basic coverage amount as well as $10,000 if you have option A.

If you lose one limb from an eligible event, AD&D will pay out ½ of your Basic coverage amount and $5,000 if you have option A.