How much do you need in your TSP for a great retirement?

1 Million? 2 Million?

Or 200k or 500k?

Every “expert” seems to have a different answer.

And it is all very different for federal employees who also have pensions, Social security, and more.

This is how you can know if you have enough for your retirement.

Your Foundation

As a federal employee you have at least 2 fixed income sources: FERS Pension and Social Security.

Note: If you retire before age 62 then you may have the FERS Supplement instead of Social Security at the beginning of your retirement. But the principles that we’ll discuss below will apply to the FERS Supplement just like it does for Social Security.

Your fixed income sources provide the foundation to your retirement.

The first step is to get an estimate of your fixed income sources.

You can get an estimate of your Social Security by making an account at SSA.gov and requesting a statement. The closer you are to retirement the more accurate your social security statement will be.

For your FERS pension, you can request an estimate from your HR. They will either run an estimate for you or provide you with software you can use to run your own estimate.

And while your gross Social Security and Pension is important, the number that is most important is your net social security and pension. AKA, how much is left after taxes and all other deductions.

The major deductions that may come out of your social security are Medicare premiums and taxes. However, if you aren’t on Medicare then of course you won’t have a Medicare premium deduction.

The main deductions for your pension will be survivor benefits, insurance premiums (health, life, dental/vision, LTC), and taxes.

Once you know what your net social security and pension will be then you can move on to the next section.

TSP Paychecks

Having 500k in your TSP is great but you have to have a system to turn that 500k into consistent paychecks in retirement.

The 4% rule is one way to do this.

The 4% rule is a system to help you know how much you can spend every month from your TSP without worrying about running out.

4% Rule Explained

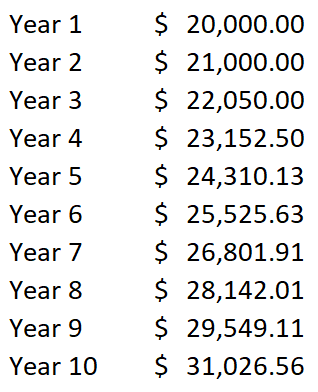

If you have 500k in your TSP then the 4% rule says you can spend 20k (4% of your balance at retirement) in the first year of retirement.

And in consecutive years you can spend the 20k plus whatever inflation was the previous year.

So if inflation in year 1 of retirement was 5% then you could withdraw $21,000 in year two.

And if inflation was 5% every year for the first 10 years of retirement then your withdrawals would look like this:

Is 500k Enough: Example

Simply put, 500k is enough if you are okay with 20k/year of withdrawals adjusted for inflation overtime.

If you need more than that from your TSP then you probably aren’t ready to retire.

But here is an example to walk you through how to do the math for you.

Let’s say that your net (after taxes and deductions) pension and social security are as follows:

Pension: $1,500

Social Security; $2,000

Total Fixed Income per month: $3,500

And if you have 500k in your TSP then we know you can withdraw 20k/year which is $1,666/month.

But your TSP is probably mostly in the traditional (pre-tax) TSP which means that you’ll have to pay taxes on the $1,666. So your net amount may look like this:

Gross Monthly TSP withdrawal: $1,666

Taxes: $250

Net Monthly TSP Withdrawal: $1,416

So your total net income in retirement would be about this:

Fixed Income: $3,500

TSP Income: $1,416

Total: $4,916

In this example, you’d have $4,916/month of net income in retirement. But again, the question is, is that enough?

My go-to strategy to figure out if that is enough for you is to compare it to what you are taking home from your job right now.

To do this, pull out a pay stub and look at your net pay.

For this example, let’s say your net pay is $2,000/pay period (every two weeks).

The first thing we need to do is to change this from a bi-weekly number to a monthly number.

We do so by multiplying by 26 (the number of pay periods in a year) and dividing by 12.

$2,000 x 26 = $52,000 / 12 = $4,333

This means that if you are taking home $2,000/pay period then that is about $4,333/month.

And if you are currently living off of $4,333/month comfortably then having $4,916/month in retirement will probably be comfortable as well.

Final Thoughts

Everyone has a different idea of what a comfortable retirement looks like for them, however, comparing what you’ll have in retirement to what you are taking home now is a great way to see where you stand.

Planning for retirement can feel overwhelming but I promise you will thank yourself over and over for all the time and energy you put into being prepared.