HR pension estimates are one of the most important documents that help you make sure you’re prepared for retirement.

However, it is very common for these estimates to have mistakes.

When federal employees rely on these estimates without checking them, they can run into big problems down the road.

In this article we’re going to look at the common mistakes to look out for and how you can adapt accordingly.

Taxes

The vast majority of your pension is taxable income. Therefore, there is going to be a tax withholding that comes out of your pension payment every month.

But on almost all the pension estimates that I’ve seen, the estimate for taxes is way too low!!

Most pension estimate softwares assume that the only income you’ll have in retirement is your pension. However, for most feds, this is simply not the case.

Most feds have other income sources as well like Social Security, TSP withdrawals, military retirement, etc. And these other income sources often mean that more tax needs to be taken out of your pension.

So the after-tax ‘Net Pension’ amount may be smaller than your pension estimate says it will be.

Choices, Choices

What your Net Pension will actually be will also depend on the elections you make including: survivor benefits, FEGLI, FEHB, & Dental/Vision.

For example, for survivor benefits, you have the option to elect survivor benefits for your spouse. If you do, your pension can be reduced by 5% or 10% depending on which option you select. For more information on this, check out this article.

Also, if you choose to keep your insurance (health, life and/or dental/vision) into retirement then you’ll have to pay the premiums from your pension.

So make sure your HR’s pension estimate is making the right assumptions about the elections you’ll make in retirement so you know exactly what will be deducted from your pension every month.

Assumptions

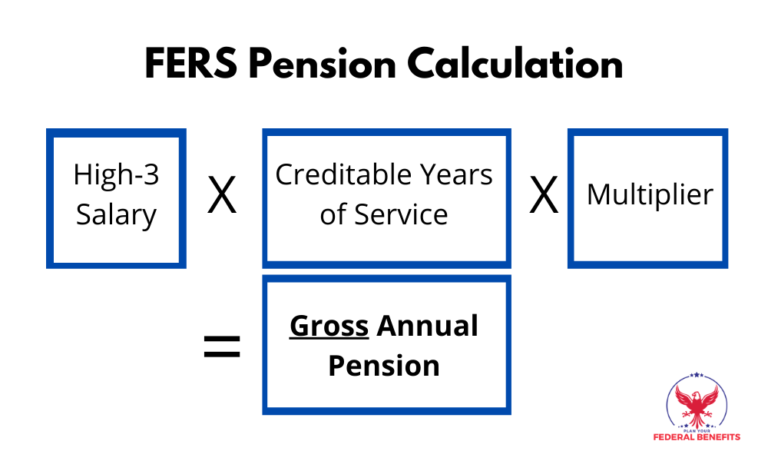

There are three things that go into your gross pension calculation: High-3 Salary, Creditable Years of Service and your Multiplier. Here is a the formula:

Your HR can easily get any of these three variables incorrect if they don’t understand everything about your career.

High-3 Salary

Your high-3 salary is the first component of your pension calculation. Put simply, your high-3 is your highest average salary during 36 consecutive months of your career.

For many people, their high-3 comes from the last 3 years of their career because that is when they got paid the most. That being said, it is important to know that it doesn’t have to be the last 3 years of your career. Your high-3 will automatically be the 3 years that you had the highest pay regardless of when it occurred in your career.

Sometimes, when people get their HR pension estimates, your HR doesn’t understand that you’re going to be working for a couple more years or that you’re going to be accepting a promotion that pays higher and your High-3 salary will actually be greater than they estimated.

Years of Service

Since you experienced your career, you know exactly how many years of service you have. But your HR may not be on the same page.

This could be especially true if years of service weren’t documented properly or you changed agencies and your records were not sent over.

Make sure your actual years of service is what they have in their calculation. For more information on how to calculate your years of service, check out this article.

Multiplier

Your multiplier will be 1% unless you retire at age 62 or older with at least 20 years of service, at which point your multiplier would be 1.1% (a 10% raise!).

Make sure your HR gets your multiplier correctly especially if you have more or than a 1% multiplier.

Retirement Date

And just to be safe, make sure your pension estimate is for your actual planned retirement date as a small change in dates can mean a big change in your benefits.

Conclusion

Nobody cares more about your retirement than you. Make sure things are right!

Your HR might be the best HR in the world. But, they don’t know your career as much as you do. Take initiative to make sure you’re set for retirement.