The L funds are a very popular choice especially now that they are the default investment for new employees.

Consequently, a question that I get all the time is, “Which L fund is the best?”

And while there is certainly not a “Best” option, there are dramatic pros and cons between the different L funds.

Here is a list of the current L funds.

-L Income

-L 2025

-L 2030

-L 2035

-L 2040

-L 2045

-L 2050

-L 2055

-L 2060

-L 2065

L Fund Basics

The first thing to understand when investing in the L funds is what they are designed to do.

In essence, the L funds are not unique funds but are simply a mixture of the 5 core funds (C, S, I, F, and G).

The TSP created the L funds in efforts to simplify investment decisions for federal employees. Many feds who were unfamiliar with the 5 core funds , struggled to know which mix they should use.

The idea is that federal employees can simply put their entire TSP balance into the L fund that is closest to their projected retirement date and then leave it for a long time. And as time goes on, the L funds automatically invest themselves more conservatively as people approach retirement.

As the target date for each fund is passed, it becomes the L Income fund. This just happened to the L 2020 fund.

Example

For example, if John Smith was planning to retire in 2035, he’d invest his entire TSP in the L 2035 fund and let it ride. Over the next 15 years, the L 2035 fund would slowly become more conservative (more G and F fund) until it became the L Income fund.

So Which is The Best?

If someone is looking for the L fund that has the potential to earn the most over time, it will always be the one with the furthest target date. Right now, that would be the L 2065 fund. But this will also be the L fund that has the most volatility.

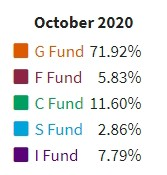

As of October 2020, the L 2065 was split up like this:

As you can see, this fund has very little G and F in it. It is meant for those federal employees that have a long-time time horizon.

The L Income fund is on the other side of the spectrum and is very conservative. Here is the allocation for the L Income fund:

Since most of the L Income fund is in the G fund, this fund is very unlikely to lose money. That being said, this fund is also very unlikely to earn much over time.

Retirees especially will want to find a balance between being too conservative or too risky so that they don’t outlive their money but they also can make it through the next market downturn.

Conclusion

The L funds can be a great tool for many federal employees. The most important thing is that you understand what the L funds are going to do over time and to make sure that it makes sense for you now and in the future.