Navigating retirement successfully requires a thoughtful approach to managing your Thrift Savings Plan (TSP). Your TSP, built over years of saving and investing, can provide a steady stream of income in retirement if you adopt strategies tailored to your needs. This article will cover two useful strategies to consider: the Bucket Strategy, and the 4% Rule.

Retirement Investment Strategy

In my opinion, the 2 goals of any good retirement investment strategy should be:

Make sure the money that you’ll need in the short term is safe.

Make sure that your money grows, beats inflation, while allowing you to maintain your standard of living throughout your entire life.

The goal of both the bucket strategy and 4% rule is to do exactly that.

The Bucket Strategy

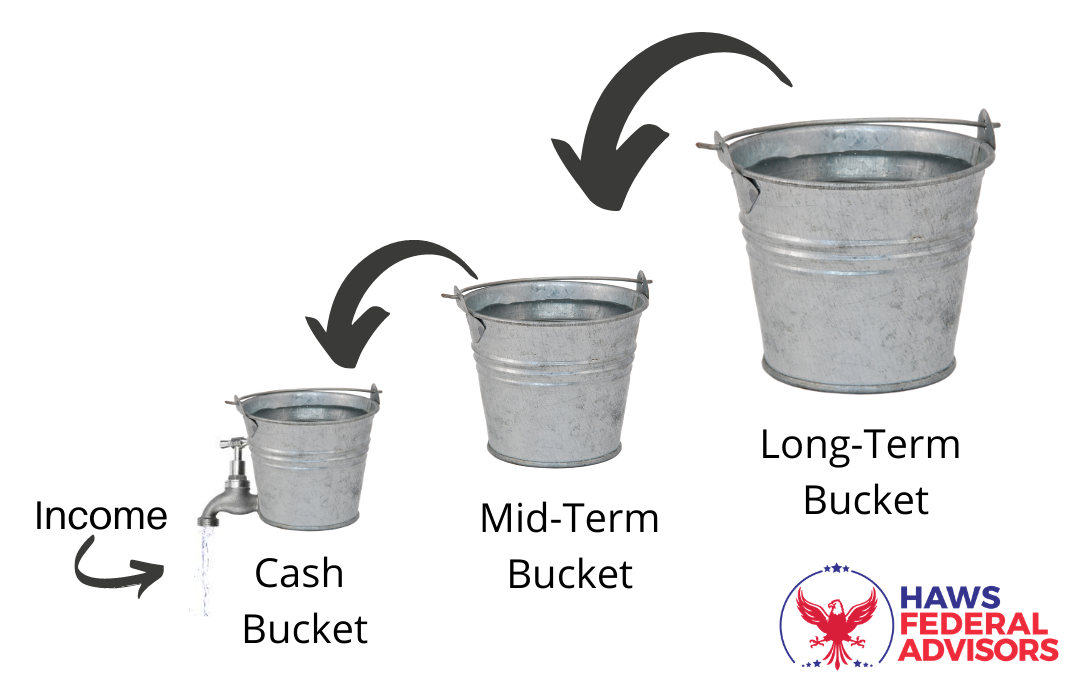

A great way to think about retirement investing is to break it down into buckets or timeframes. And then you would assign a dollar amount to that timeframe based on how much you’ll need from your investment during that time.

For example, split up your retirement into 3 different buckets. A cash bucket, mid-term bucket, and long-term bucket.

As the picture shows, the cash bucket is where you get your “paychecks” in retirement or in other words, where you take distributions from. But how much money do we put in each bucket? Great question. A good rule of thumb is 2-4 years worth of needed income in the cash bucket, the next 2-4 years of income in the mid-term bucket, and any money that you’d need after that can go into the long-term bucket.

How to Invest Each Bucket?

The reason we split up your retirement into different buckets is so that you can tailor your investment strategy for that time period. The cash bucket is designed to cover your income needs in the very short term so you want this money to be in cash or cash equivalent. The G fund can often be a great choice for this bucket. The G fund won’t grow much but it will provide the stability that you need in the short term.

Often a good choice for the mid-term bucket is bonds (the G and F funds). These funds will grow faster than your savings account but are much more stable than the stock market.

And any money that is not in the first two buckets will go into your long-term bucket. This bucket should be invested in funds that will provide the growth that you need over time. The C, S, and I funds often make a lot of sense in this bucket.

As a result of the first two buckets, you now have about 4-8 years worth of retirement income that will be there for you regardless of what the stock market does. This means that even if the stock market gets cut in half on the day you retire, you have 5 years worth of income before you even have to think about selling your stock-based funds (C, S, and I) when the market is down.

This strategy gives the market plenty of time to recover at which point you can refill your cash and mid-term buckets. So just like any good retirement strategy should, this bucket strategy successfully protects your short-term needs while also providing the growth that you need to maintain your standard of living over time.

The 4% Rule

The 4% Rule is another widely used strategy to manage withdrawals from your TSP. It provides a guideline for how much you can withdraw annually without depleting your retirement savings.

How It Works

This rule suggests that in the first year of retirement, you can withdraw 4% of your total TSP balance. In subsequent years, you adjust this amount for inflation. For instance:

If you have $500,000 saved in your TSP, you could withdraw $20,000 in the first year.

In year two, if inflation is 5%, you would withdraw $21,000.

Historically, this approach has assumed a balanced portfolio of 50% stocks (C, S, and I Funds) and 50% bonds (G and F Funds). But, most financial experts disagree with this portfolio and advise a more aggressive one.

Benefits

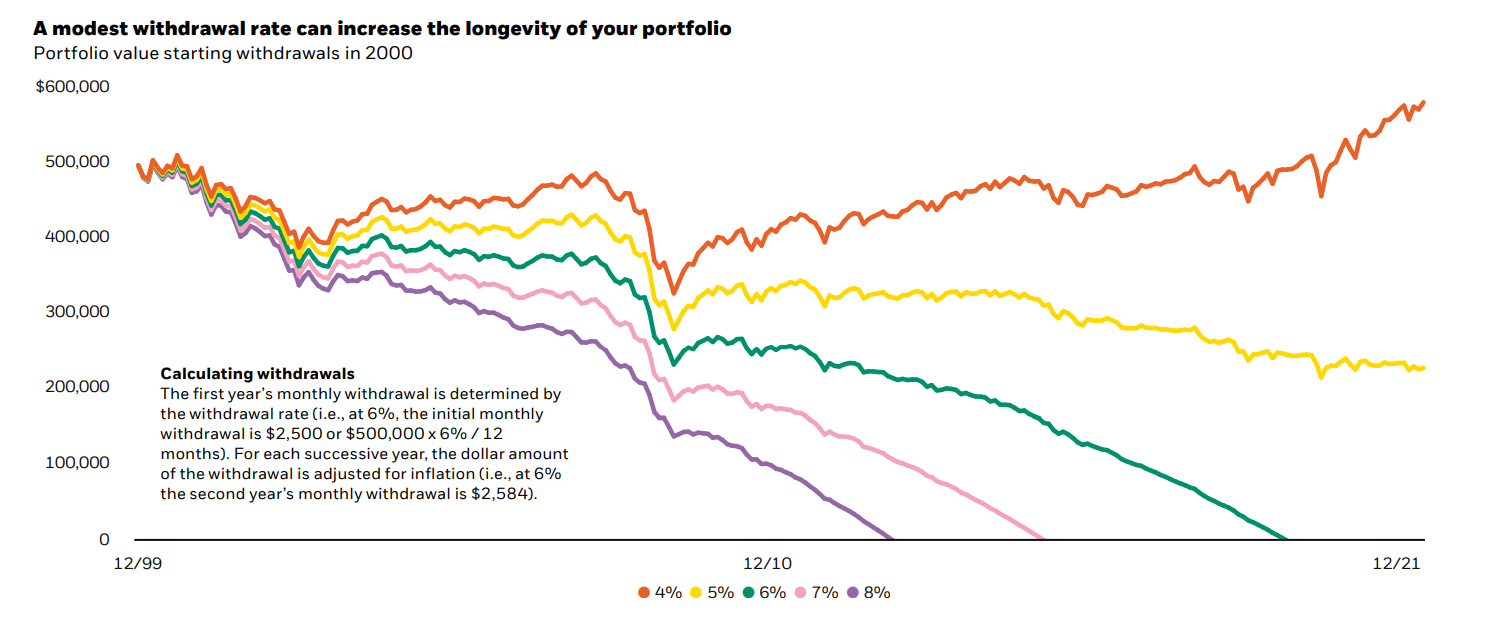

The 4% Rule ensures a sustainable withdrawal rate. Historically, retirees following this rule have a high probability of not running out of money, even during challenging market periods. It’s a conservative approach that provides a stable income while allowing your remaining investments to grow over time. Here is a graph of the 4% rule compared to other percentages starting in the year 2000:

Considerations

Some criticism of the 4% Rule is that it can be overly cautious in favorable markets, potentially leaving money on the table. However, its strength lies in its reliability across different economic conditions, making it a solid baseline strategy for most retirees.

How to Use The Bucket Strategy & 4% Rule Together

In the first year of retirement, calculate 4% of your total TSP balance to determine your initial withdrawal amount. Then, use your cash bucket (the first bucket) to fund this withdrawal. For example, if your TSP balance is $500,000, the 4% Rule suggests you can withdraw $20,000 in the first year. This withdrawal comes entirely from the cash bucket, which is designed to provide your “paycheck” in retirement.

Let’s assume you are very conservative and you want to have 4 years worth of TSP withdrawals in your cash bucket and another 4 years worth of TSP withdrawals in your mid-term bucket. That’s a total of 8-years worth of money in conservative investments like the G & F funds. Using the 4% rule, you would need 32% (8 years x 4%) of your TSP in conservative investments. The rest (64%) would be invested in more aggressive funds like (C, S, & I funds).

As you adjust your withdrawal for inflation in subsequent years, you can replenish your cash bucket by moving funds from the mid-term bucket. When markets are strong, you can sell equities from your long-term bucket (C, S, and I Funds) to refill the mid-term bucket, ensuring your overall portfolio stays aligned with your goals. This structure allows you to stick to the 4% Rule while giving the market time to recover after downturns, reducing the likelihood of selling stock-based funds during unfavorable periods.

Not All People Need This

Everybody’s retirement situation is different. Some people can live just fine off of other sources of income such as their FERS (Federal Employee Retirement System) pension, FERS supplement, social security, rental income, etc. When people don’t plan to withdraw from their TSP in retirement, using the 4% rule and having short to mid-term buckets sometimes doesn’t make sense. Whether you’re withdrawing from the TSP or not, make sure you have a plan at retirement. If you would like professional help, feel free to schedule a meeting with us here: https://app.hawsfederaladvisors.com/whatservicemakessense