When it comes to federal retirement, the terms “postponed” and “deferred” might seem interchangeable at first glance. After all, they both involve delaying the start of pension benefits. However, there are important distinctions between the two, especially when it comes to eligibility, benefits, and the ability to retain health insurance. Understanding the differences between postponed and deferred retirements can help you make the best decision for your career and future.

What is Deferred Retirement?

Deferred retirement is an option for federal employees who leave government service before reaching the age required for an immediate retirement, yet still want to receive a pension at a later age. To qualify for a deferred retirement under the Federal Employees Retirement System (FERS), employees must meet two key criteria:

At least 5 years of creditable service (which can include part-time work, military service, or civilian service under the federal government).

Leave their FERS retirement contributions in the system. This is crucial because employees who choose to withdraw their contributions are not eligible for a deferred pension.

How Deferred Retirement Works

The key feature of a deferred retirement is that it allows the employee to leave the federal workforce and “defer” the collection of their pension benefits until they meet the eligibility age. Here’s a breakdown of how the pension is calculated and when payments begin based on the length of service:

With 5 years of service, you can begin your pension at age 62.

With 20 years of service, your pension can begin at age 60.

With 30 years of service, you can begin your pension at your Minimum Retirement Age (MRA). For most people, their MRA is 57 years.

Major Drawbacks of Deferred Retirement

While deferred retirement can be a flexible option, it comes with several notable downsides, especially for individuals with shorter service years. One major drawback is the reduced pension amount for those who begin collecting it early. Additionally, federal employees who opt for a deferred retirement lose access to key benefits that many rely on, including:

Federal Employees Health Benefits (FEHB): Deferred retirees are not eligible to keep their health insurance into retirement. This can be a significant financial burden, especially since healthcare costs for retirees can be high.

Federal Employees Group Life Insurance (FEGLI): Deferred retirees are also ineligible for this program.

FERS Supplement: Unlike those with other retirement options, deferred retirees do not receive the FERS supplement, which helps bridge the gap between retirement and when Social Security benefits begin.

Reductions to Your Deferred Retirement

If you have at least 10 years of service then you’d be able to start your deferred pension as early as your minimum retirement age but with a reduction.

Basically, you’ll see a 5% reduction to your pension for every year you take it before you’d otherwise be eligible. For example, with only 10 years of service you’d see a 25% reduction (5% for each of the 5 years) to your pension if you started it at 57 instead of 62. But if you would have had 20 years of service then you’d only see a 15% reduction because there is only 3 years between age 57 and age 60 (when you’d otherwise be eligible with 20 years of service).

What is Postponed Retirement?

Postponed retirement, on the other hand, is a retirement option available to employees who are eligible for MRA+10 retirement but choose to delay their pension benefits until a later time. To qualify for a postponed retirement, federal employees must meet the following requirements:

At least 10 years of service.

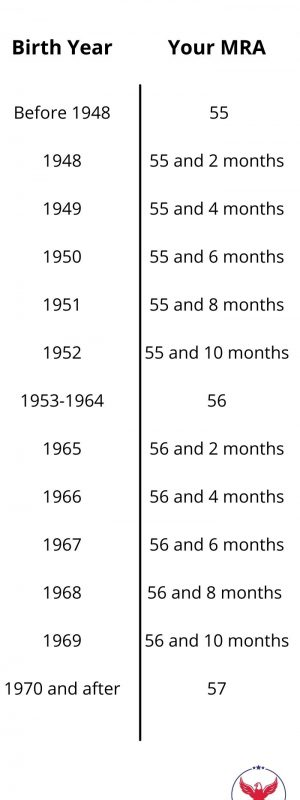

Reached the MRA, which is determined based on the employee’s birth year. Here is a table:

Unlike deferred retirement, postponed retirement allows employees to keep their health insurance (FEHB) and life insurance (FEGLI) benefits into retirement. This can be a significant advantage for those who rely on government-provided health benefits.

How Postponed Retirement Works

A key feature of postponed retirement is the flexibility it provides. Employees eligible for MRA+10 retirement can choose to retire and postpone their pension to a later date, usually until they reach age 62. By postponing their pension, they avoid the permanent reduction that would otherwise occur if they began collecting their pension early.

For example, consider an employee who reaches their MRA at age 57 with 10 years of service. If they choose to retire at that time and start collecting their pension immediately, they would face a reduction of 25% (5% per year before age 62). However, by postponing their retirement until age 62, they would receive 100% of their pension without any reduction.

Deferred vs. Postponed Retirement: Key Differences

Conclusion

While both deferred and postponed retirements offer federal employees the ability to retire before the traditional age of 62, the key differences lie in eligibility and the ability to keep benefits like health insurance. If you qualify for a postponed retirement, it is generally a better option due to the ability to avoid pension reductions and retain health coverage.

However, if you’re considering retiring early and you don’t need immediate access to health insurance or other benefits, a deferred retirement may be a viable option for you. As always, it’s important to consider your individual circumstances, including health needs, financial goals, and career plans before making a decision.

Understanding the distinctions between these two types of retirement can help you plan more effectively for your future. Whether you choose a deferred or postponed retirement, it’s critical to ensure that you’re making an informed decision based on the long-term impact on your financial security and healthcare. Check out our website for more information about federal retirement: https://hawsfederaladvisors.com/