What sets apart those that are extremely well prepared for retirement from those that may be cutting it close?

In my experience, it is often debt (the lack of) and the TSP (Thrift Savings Plan).

And while keeping debts to an absolute minimum (i.e. paying off your mortgage etc.) is an incredibly important topic, I am going to focus my attention today on the TSP.

Your TSP: The Difference Maker

Federal employees enjoy 3 main sources of retirement income: FERS pension, Social Security, and the TSP.

And of the 3, your pension and Social Security tend to take care of themselves as you have limited control over them outside of when you choose to retire.

Which leaves the TSP as your main retirement tool left almost completely in your control.

And this is why the TSP is often the difference between those that retire confident and those that don’t.

Maximizing your TSP (Thrift Savings Plan)

There are 3 main levers you can pull in getting the most out of your TSP.

They are:

Deciding how much to contribute to the TSP

If you want to learn more about the first two, feel free to hit the links above because in this article we are focusing on #3.

How Much You Should Be Saving Into Your TSP

It can be hard to know exactly how much you should be saving for retirement.

Because of this, some people like Dave Ramsay use 15% of your income as a rule of thumb for how much you should put aside.

However, this number will certainly change depending on your other income sources and income level.

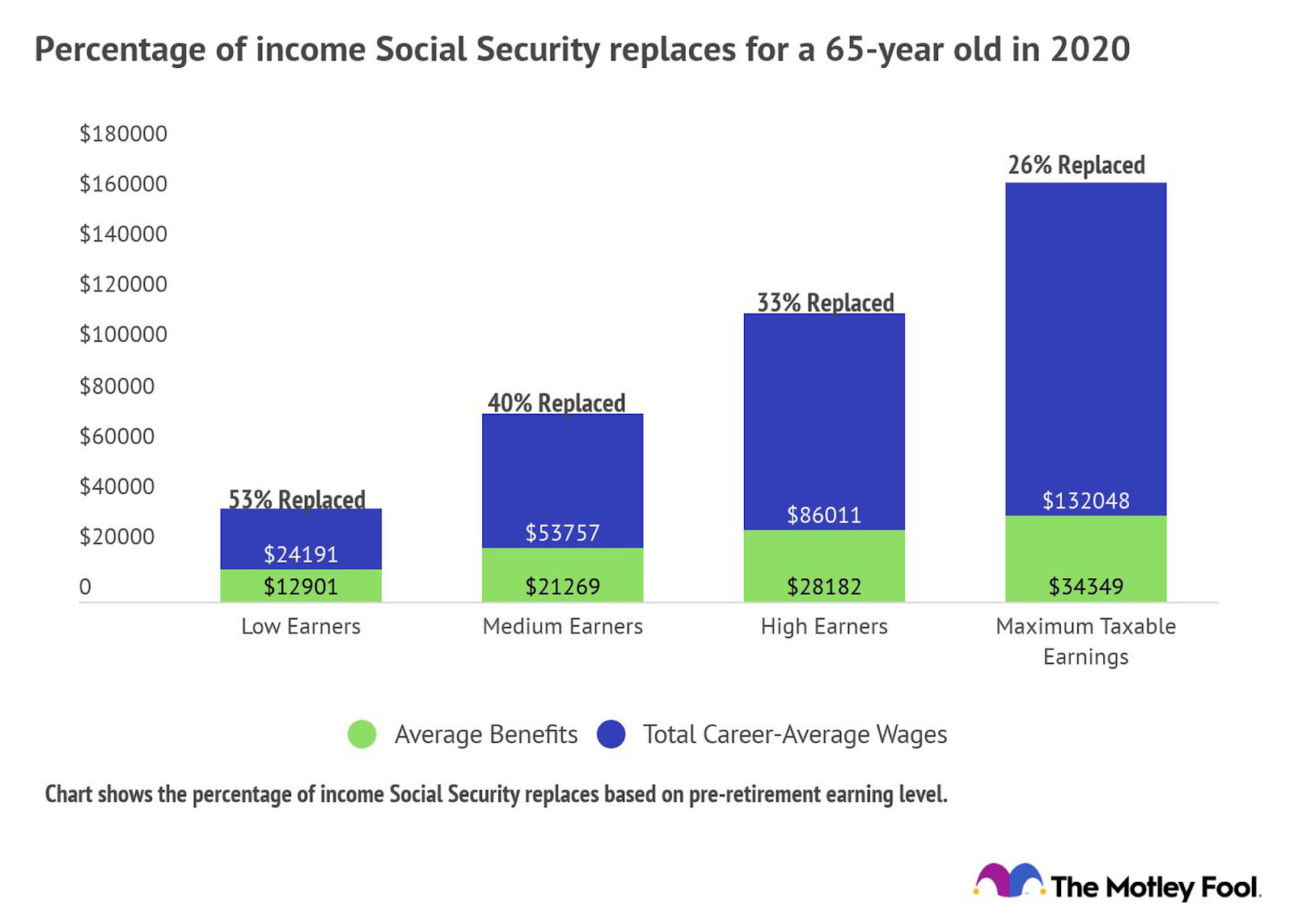

For example, per the chart below, the higher your income level, Social Security will replace a smaller and smaller percentage of your income in retirement.

Note: Higher earners tend to have higher Social Security benefits but as a percentage it is often a small percentage of their pre-retirement income.

source:https://www.fool.com/investing/2020/11/18/how-much-of-your-pre-retirement-income-will-social/

This means that the higher your income, the more you’ll need to be putting aside in your TSP to cover a higher percentage of your income in retirement.

But ideally, as your income increases, so does your ability to save more for retirement.

What Are Your Retirement Goals?

But again, because your TSP will be funding your retirement you will want to be based on your goals. For example, some people want to enjoy more money in retirement then they had during their careers.

If this is the case, then you’ll put even more aside to make that happen.

As Much As You Can

So as you can see, there are lots of things that can impact how much you should be saving (not even talking about how the stock market performs) so it is almost impossible to nail down an exact percentage.

However, you should always start by saving as much as you can. And then from there try to save more as you get raises or pay off other debts.

And of course you don’t want to sacrifice all the niceties of life before retirement but anything extra you can do will make a big difference in the long run.