Required Minimum Distributions (RMDs) can be a significant consideration for federal employees nearing retirement. At first glance, the RMD rules may appear daunting. RMDs are mandatory withdrawals from retirement accounts starting at a certain age, with tax implications that could potentially alter a retirement plan. However, with proactive planning and a clear understanding of strategies to manage RMDs effectively, federal employees can navigate these requirements in a way that aligns with their financial goals and minimizes tax impacts.

What Are RMDs?

Starting at certain ages, the government requires that you withdraw a portion of your traditional TSP every year. Why do they do this? Because they want to get a piece of the action. Basically, whenever you withdraw money from your traditional TSP account that is when you pay taxes. So RMDs force you to start withdrawing instead of keeping your money within the TSP (with taxes unpaid) indefinitely.

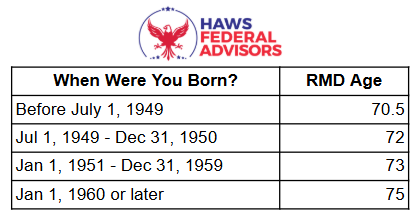

When Do RMDs Start?

The table below shows when RMDs start for you:

For example, if you were born in November, 1953 and you are turning 73 in 2026 then this is what your RMD calendar would look like:

RMDs continue perpetually until you have no remaining funds in traditional accounts.

How Much Do I Have to Take out of My TSP for RMDs?

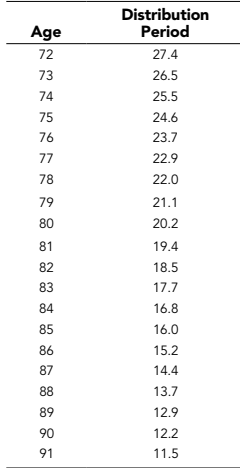

The simple answer is that the amount you have to withdraw is based on your age and the withdrawal percentage gets bigger as you get older. The longer answer is that the amount is based on a chart like the one below. Once you find your age on the chart then you divide your TSP balance by the distribution period.

For example: If you had $500,000 in your traditional TSP account and you turn 75 this year, your RMD would be $500,000 / 24.6 = $20,325.

Note: These numbers and charts are updated over time and I can’t promise to have this post updated every time there is a change so you will want to make sure you are using the right numbers!!!

Do RMDs Apply to My Roth Accounts?

No, RMDs do not apply to Roth accounts. Because of the Secure Act 2.0, your Roth TSP is not subject to early withdrawals. Your Roth IRA is not subject to RMDs either.

How to Minimize Taxes on RMDs

Managing the tax impact of RMDs will require you to plan ahead. Here are some ways federal employees can mitigate tax consequences:

Roth Conversions Before RMDs Begin: One effective strategy to reduce future RMDs is converting a portion of your traditional TSP or traditional IRA funds into a Roth IRA before reaching the RMD age. Since Roth accounts are not subject to RMDs, transferring funds this way will help avoid mandatory distributions and the associated taxes. However, Roth conversions themselves trigger taxes on the amount converted, so it’s important that you calculate the impact and consider spreading conversions over several years if needed. Spreading out your roth conversions over more years will reduce the total amount of taxes paid.

For example: Let’s say you have just retired at the age of 62 and have $500,000 in your traditional TSP account. Instead of waiting for RMDs to start, you could begin now by converting small percentages of your traditional TSP to a Roth IRA. Check out this video to learn how to do that. You should also take into consideration your tax bracket and how much extra income you can have before you move up into the next tax bracket.

Begin Withdrawals From Your Traditional Accounts First: To ease the tax burden, some federal employees may consider taking distributions from their traditional accounts first. Much like Roth conversions, this approach can help spread the tax impact over several years rather than concentrating it once RMDs become mandatory. This can also help your Roth accounts (if you have any) to grow faster and tax-free (we like this).

Strategic Charitable Contributions: If philanthropy is part of your retirement plan, consider making Qualified Charitable Distributions (QCDs) directly from your IRA to a qualified charity once you turn 70½. QCDs are not available through the TSP. QCDs can count toward satisfying your RMD for the year and can reduce your taxable income since these distributions are excluded from your adjusted gross income (AGI). This strategy can be particularly useful for federal retirees who want to minimize the effect of RMDs on their tax liability while supporting causes they care about.

What Happens If You Don’t Take an RMD from Your TSP/IRA?

We know how serious Uncle Sam is about something by how badly they penalize those that don’t follow along. And when it comes to RMDs, Uncle Sam is very serious. If you fail to take an RMD then you will owe a 50% penalty on your missed RMD. For example, if you were supposed to withdraw $30,000 as an RMD last year but you didn’t (or just forgot) then you’d have to pay a $15,000 penalty!

But I have some good news. The TSP will automatically withdraw your RMD for you at the end of the year if you don’t do it yourself. This means that TSP has your back if you forget in a given year but I would certainly still keep an eye on it if I were you. Note: If you have money in an IRA then you are often on your own to make the RMD happen so you’ll want to make sure you are withdrawing at least your RMD each year.

Conclusion

RMDs don’t have to be scary. As we observed, there are ways to prepare in advance to get the most out of your hard earned money.

If you haven’t planned ahead and are about to start RMDs, don’t worry. Although you might have to pay more taxes over time, you can still implement these strategies to reduce taxes. If you have more questions or would like professional help, feel free to schedule a meeting with us here: https://app.hawsfederaladvisors.com/whatservicemakessense