Do you enjoy saving 30%-40% on medical expenses you’re already planning to pay for? If so, it’s time to take a closer look at Flexible Spending Accounts (FSA) and Health Savings Accounts (HSA). These powerful tools can help federal employees reduce taxes while covering healthcare costs.

However, understanding the key differences between an FSA and an HSA is crucial. Many people miss out on maximizing their savings simply because they don’t know how to optimize these accounts. Let’s dive into what these accounts offer and how to choose the right one for you in 2025.

Why FSAs and HSAs Matter

Both FSAs and HSAs allow you to pay for medical expenses with pre-tax money, which means you save on income tax, Social Security tax, and Medicare tax.

For example, if you need $1,000 for medical expenses, paying with after-tax dollars means you’d have to earn up to $1,500 (depending on your tax bracket). Using pre-tax dollars through an FSA or HSA lets you pay the $1,000 directly, saving $500 or more.

While these accounts share tax advantages, their differences significantly impact how you use and benefit from them.

What Is a Flexible Spending Account (FSA)?

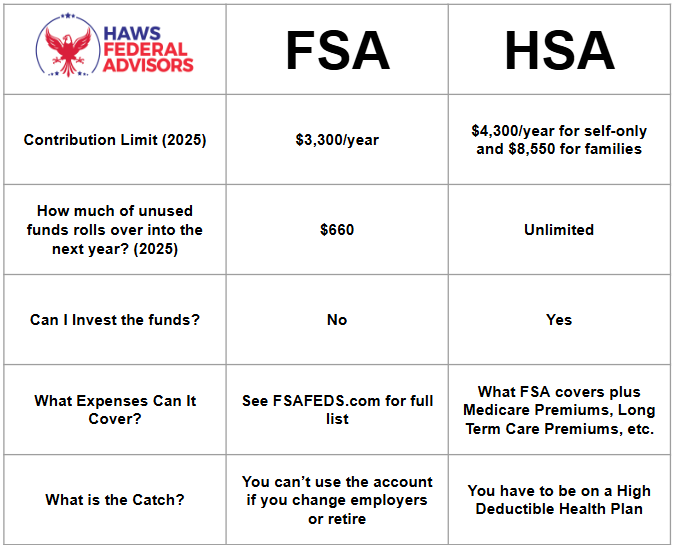

Contribution Limits: In 2025, the annual contribution limit for FSAs is expected to increase to $3,300 (up from $3,200 in 2024).

Rollover Rules: FSAs are “use-it-or-lose-it” accounts, meaning you can only roll over a limited amount—$660 in 2025—into the next year. Unused funds beyond that limit are forfeited (it will go back to the employer).

Eligible Expenses: FSAs cover a broad range of expenses, including:

Medical: co-pays, deductibles, and coinsurance.

Dental: cleanings, braces, and X-rays.

Vision: eyeglasses, contacts, and laser surgery.

Professional services: physical therapy and chiropractic care.

Prescription drugs, insulin, and prescribed over-the-counter medicine

Over-the-counter health care items: bandages, pregnancy test kits, blood pressure monitors, etc.

Investment Options: FSAs don’t allow investment options/growth. Funds are meant to be spent during the plan year.

Portability: FSAs are tied to your employer. If you retire or change jobs, you forfeit any remaining funds.

What Is a Health Savings Account (HSA)?

Contribution Limits: For 2025, HSAs allow contributions of up to $4,300 for individuals and $8,550 for families. Those aged 55 and older can add an extra $1,000 as a catch-up contribution.

Rollover Rules: Unlike FSAs, HSAs don’t have rollover limits. Any unused funds stay in your account indefinitely, making it an excellent option for long-term savings.

Eligible Expenses: HSAs cover all the same expenses as FSAs, plus additional categories like:

Medicare premiums.

Long-term care insurance premiums.

Non-prescription services, such as massages.

Investment Options: HSAs allow you to invest your contributions, offering potential growth over time. Many federal employees use HSAs to build a tax-free medical fund for retirement.

Portability: HSAs are yours for life. You keep the account even if you switch jobs, retire, or change health plans.

What is the catch of an HSA?

So far you might have noticed that an HSA is better than an FSA in almost every way so why doesn’t everyone use it? Because not everyone can. To contribute to an HSA you have to:

Be enrolled in a HDHP (High Deductible Health Plan)

Can’t be enrolled in Medicare, Tricare, or other non-HDHP

Can’t be claimed as a dependent on someone else’s tax return

HSA vs. FSA Comparison Chart (2025)

Can Federal Employees Use Both an FSA and HSA?

Generally, FSAs and HSAs are mutually exclusive, meaning you can only contribute to one. However, a Limited Expense FSA (LEXFSA) is an exception.

A LEXFSA can be used alongside an HSA but is restricted to cover only dental and vision expenses. If you have an HSA, a LEXFSA can provide extra pre-tax savings for these categories.

Is an HSA Worth Using a High Deductible Health Plan (HDHP)?

The primary trade-off for HSA eligibility is enrolling in a High Deductible Health Plan (HDHP), which requires paying more out-of-pocket before insurance coverage kicks in. However, HDHPs often have lower premiums and may include employer HSA contributions.

The Federal Employees Health Benefits (FEHB) program offers HDHPs with competitive out-of-pocket maximums. Some plans contribute a substantial amount annually to your HSA, helping offset higher deductibles.

When Does an HDHP Not Make Sense?

While HDHPs and HSAs work well for many, they’re not ideal for everyone. For example:

If you have high, recurring medical expenses, a plan with lower deductibles might save you more.

Or if someone is on Medicare they will probably want a FEHB plan that is designed to merge with Medicare.

Key Takeaways

Maximize Savings: Both FSAs and HSAs offer significant tax advantages.

Longevity: HSAs are better for long-term savings due to unlimited rollovers and investment options.

Evaluate Your Health Needs: FSAs might be a better fit for short-term, predictable expenses.

LEXFSA: If you use an HSA, a LEXFSA can boost savings on dental and vision care.

By understanding these accounts, federal employees can make informed decisions and potentially save thousands in 2025.