When federal employees reach 30 years of service with the federal government, they usually start thinking about retirement. Three very common ages to retire as a federal employee are 57 (Minimum Retirement Age (MRA)), 60 or 62. Let’s take a look at the pros and cons of each retirement age, focusing on pension calculations, the FERS (Federal Employee Retirement System) supplement, and the 10% pension bonus.

First, let’s take a look at how the FERS pension and FERS supplement are calculated.

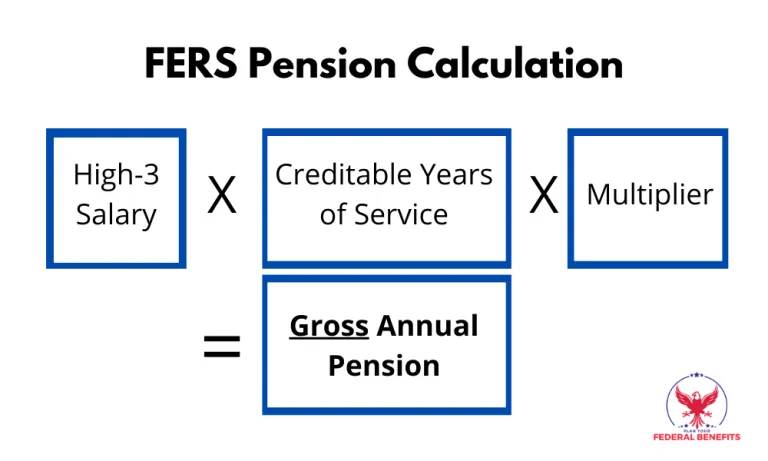

How Is My Pension Calculated?

For FERS traditional employees retiring with a full (immediate) retirement, the pension is calculated as follows:

If retiring before age 62: 1% of your average high-three salary per year of service.

If retiring at or after age 62 with at least 20 years of service: 1.1% of your average high-three salary per year of service.

Note: For special provisions, the rules are a little different. Check out this article to see how.

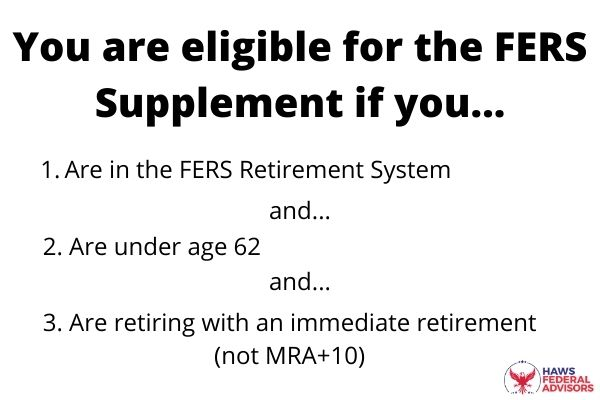

How Is My FERS Supplement Calculated?

Before you calculate your FERS supplement, make sure you are eligible for it. Here are the requirements:

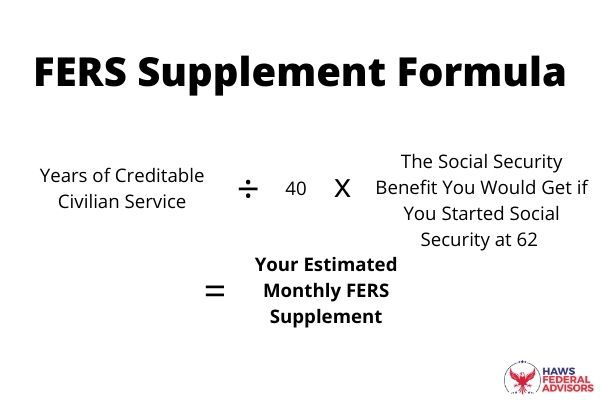

To find the value of your FERS supplement, divide your years of creditable service by 40, then multiply the answer by your age 62 SS benefits (Please take note that you can find your age 62 social security benefit at page 2 of SS statement)

Comparing Three Retirement Options (By Age)

Scenario 1: Retiring at Age 57 (MRA)

Assuming you are 57 years old, have 30 years of service, and earn a high-three average salary of $100,000. Your pension would be calculated as follows:

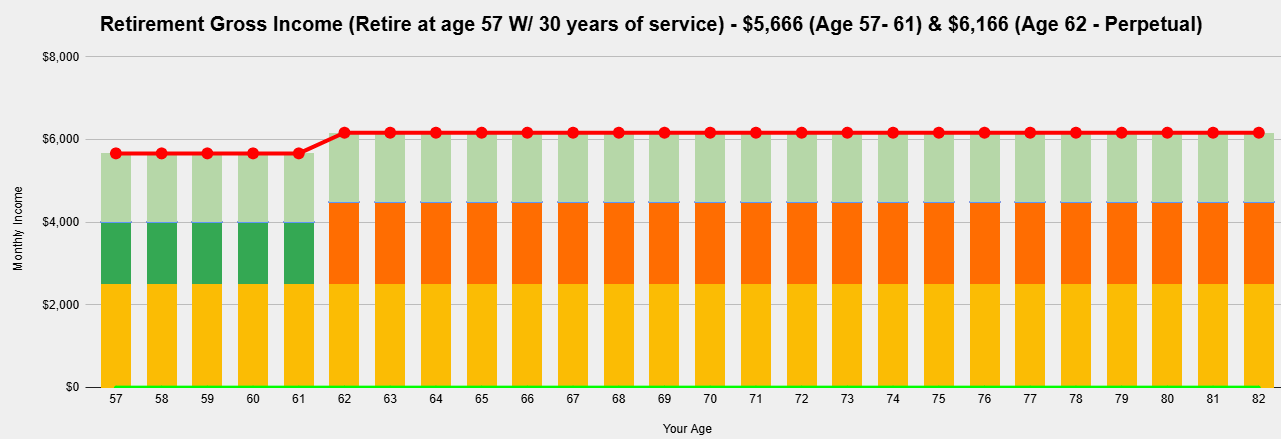

Pension Calculation: 30 years × $100,000 × 1% = $30,000 per year, or $2,500 per month.

If you retire at age 57 with 30 years of service, you would qualify for the FERS Supplement.

FERS Supplement Calculation: (Years of service / 40) × Estimated Social Security Benefit.

Assuming your Social Security benefit at 62 is estimated to be $2,000 per month, your FERS Supplement would be: 30 years / 40 × $2,000 = $1,500 per month.

This supplement would add up to $18,000 per year and would be paid until you reach age 62. Over the five-year period from ages 57 to 62, you would receive a total of: $18,000 × 5 years = $90,000.

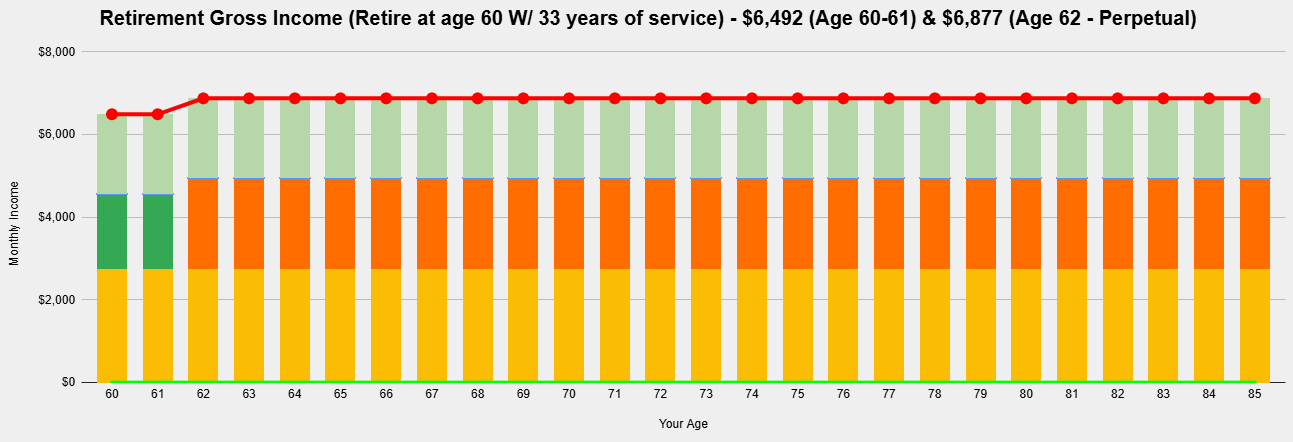

Scenario 2: Retiring at Age 60

Let’s take a look at the numbers if you waited 3 years to retire at age 60 with 33 years of service and the same $100,000 high-three average salary (although, your high-three salary would probably be slightly higher):

Pension Calculation: 33 years × $100,000 × 1% = $33,000 per year, or $2,750 per month.

At age 60 with 33 years of service, you are still eligible for the FERS Supplement. By working another 3 years, your social security benefit would probably be slightly higher. Let’s assume your social security benefit at age 62 is now $2,200. This gives a FERS supplement of: (33 / 40) x $2,200) = $1,815 per month for two years.

If you retire at age 60, you will receive the FERS supplement 2 years instead of 5. But, you will enjoy an increased pension, and social security benefit perpetually. Three years of additional service also means you have more time to contribute to your Thrift Savings Plan (TSP) and let it grow.

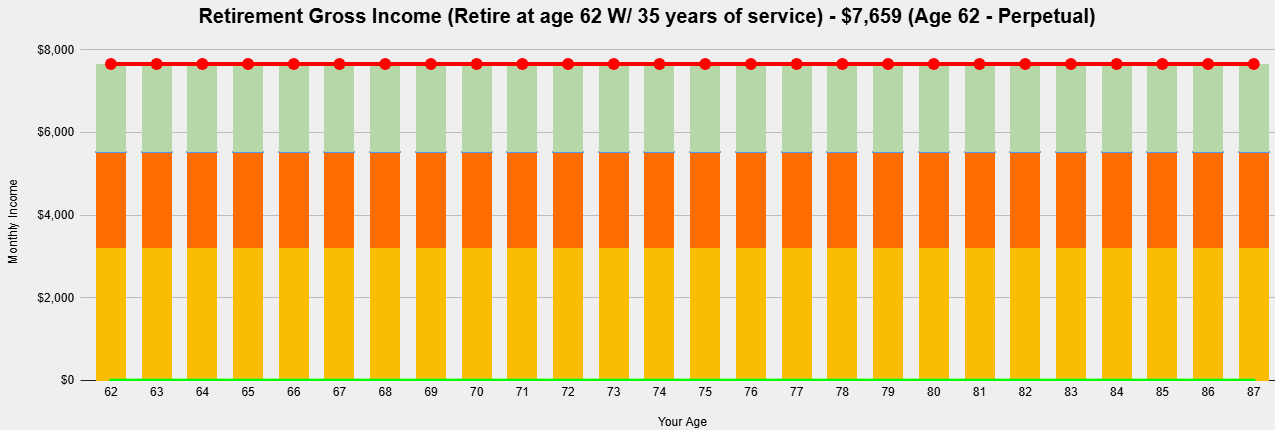

Scenario 3: Retiring at Age 62

Let’s take a look at the numbers if you waited 5 years to retire at age 62 with 35 years of service and the same $100,000 high-three average salary (although, your high-three salary would probably be higher).

If you can work until age 62, you become eligible for a 10% pension bonus, which can provide significant lifetime income increases. The pension multiplier increases from 1% to 1.1% for employees who retire at 62 with at least 20 years of service.

Pension Calculation for 35 years of service at age 62: 35 years × $100,000 × 1.1% = $38,500 per year, or $3,208 per month.

Social security benefits will increase to around $2,333 with the extra years of service.

By working until age 62, you forgo the FERS Supplement, but the increase in pension and social security is permanent and includes future cost-of-living adjustments (COLAs). Social security benefits become available at 62, providing further income options. The extra years of service also means you have more time to contribute to your Thrift Savings Plan (TSP) and let it grow.

Estimated Gross Income Graphs

Color Code:

Yellow = FERS Pension

Orange = Social Security

Dark Green = FERS Supplement

Light Green = TSP Income

These graphs assume the following:

Your High-Three salary is $100,000 (although, your high-three salary would probably be slightly higher the longer you work)

You start receiving social security at age 62

You have $500,000 in your TSP at age 57

You contribute $5,000 to your TSP each year from ages 57-62 if you’re still working

The rate of return on your TSP is 4% each year from ages 57-62

You use the 4% rule to withdraw from your TSP in retirement. For more information about the 4% rule, check out this article

Please note: These graphs are gross numbers. They do not account for taxes or deductions.

The purpose of these graphs is to give you a general idea of the different incomes you’ll receive at different ages and years of service. Everyone’s situation is unique, so do not assume this will be your income in retirement.

Summary

Retire at Age 57:

Opportunity to receive the FERS Supplement for 5 years

Lower FERS pension

Lower social security benefit

Lower TSP Amount

Retire at Age 60:

Opportunity to receive the FERS Supplement for 2 years

Higher FERS pension

Higher social security benefit

More time for TSP to grow

Retire at Age 62:

No FERS supplement

Even higher FERS pension

Opportunity for a 10% bonus to your pension

Even higher social security benefit

Even more time for TSP to grow

What is a Successful Retirement?

There are a lot of factors that contribute to a successful retirement. Perhaps the most important is not the money, but rather your happiness. Do you want to work longer to have more money or would you rather work less with less money? If you have a job that you enjoy, then maybe working a couple extra years could be a good option. If you have a job that you can’t wait to get out of, maybe working less is the better option for you.