We all love experiencing market growth when we are invested in the C, S, and I funds. These funds can be a great tool during your career and retirement. But, can there be danger when investing in these funds?

But if you are retiring soon, should you still invest in the C, S, and I funds to get more potential growth?

Uses of the C, S, and I Funds

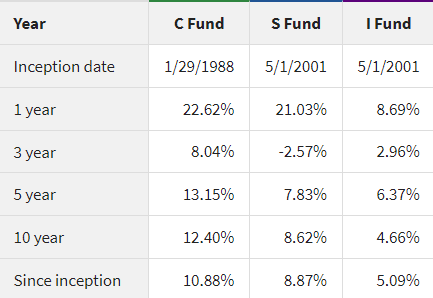

First of all, let’s take a look at the returns of the C, S, and I funds over time:

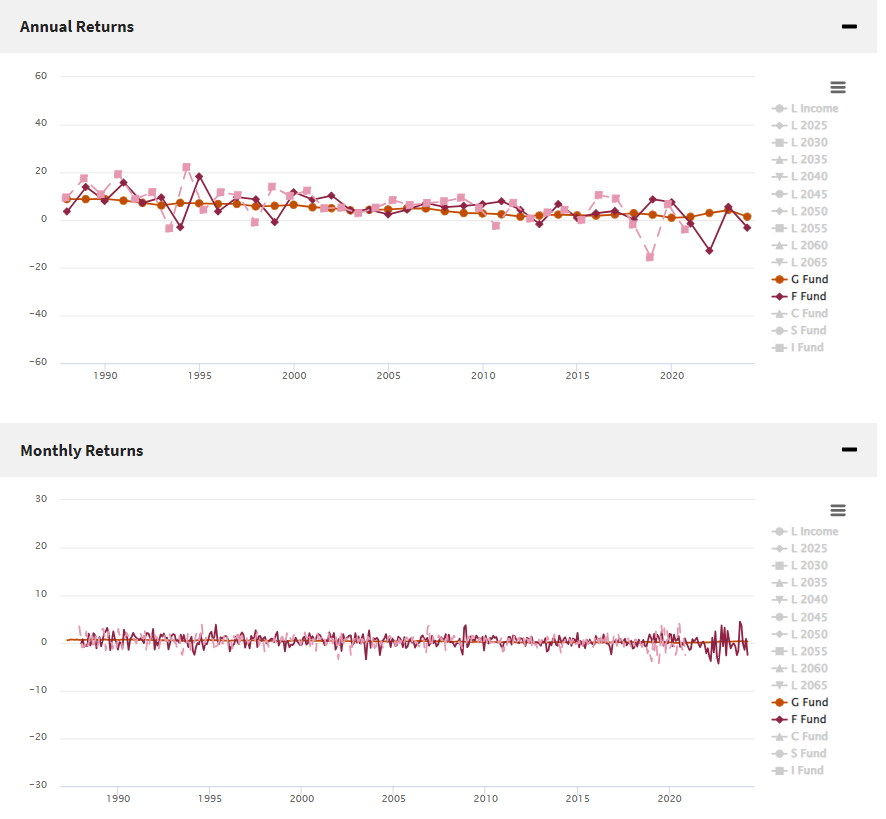

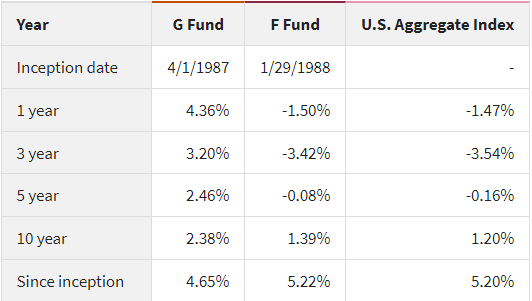

As we can see from the first two graphs, the returns on the C, S, and I funds vary a lot. Some years/months, the funds increase a lot while others do very badly. But over the years, the funds do well. As we can see from the “since inception” part of the image, the C fund has an average return of 10.88%, the S fund has 8.87% and the I fund has 5.09%. Now let’s compare them to the G, and F funds (the G and F funds are considered opposites to the C, S, and I funds):

The G, and F funds are very constant compared to the C, S, and I funds. You could pick any date to invest in the G and F funds and the returns will be very consistent. But, over time we see that the G, and F funds do not do as well as the C, S and I funds.

The strength of the C, S, and I funds is that they are great for long term growth. If you do not plan on touching your TSP for a long time, investing most of your money in the C, S, and I funds will give you the best returns over time (statistically).

Should my TSP Funds Change as I Approach Retirement?

If you are getting close to retirement, having all your TSP money invested in the C, S, and I funds can be dangerous. Why? Because withdrawing from these funds in retirement when the stock market is down, is a quick way to deplete your money.

As we saw from the graphs, there were some years that the C, S, and I funds were down by 20%-40%. Taking money from your retirement when your money is worth almost half as much can easily be a retirement destroyer.

As you approach retirement, the average retiree should have some of their money in the G and/or F funds to get them through the down years in the stock market.

What if I want a Bigger TSP Fund?

Many federal employees want to retire with as much money as they can. They maximize their FERS supplement, FERS pensions, social security, and TSP. But unlike the other three retirement benefits mentioned, the TSP is one benefit that involves risk.

In the name of “maximizing their TSP”, some federal employees invest all or almost all of their money into the C, S, and I funds even close to retirement. And maybe they’ll get lucky and have great returns. But, maybe they won’t.

I’m not saying that you shouldn’t invest in the C, S, and I funds at all as you approach retirement. I’m saying that it’s dangerous to invest all or close to all your hard earned money into aggressive funds when you’re getting close to needing that money.

What’s the Solution

Like most things, you need a balance. You need some funds in conservative investments like the G and F funds, and you need some investments in aggressive funds like the C, S, and I funds. Why both? It’s good to have money that won’t fluctuate too much over time and that can provide you with a stable income. Investing a portion of your investments in aggressive funds gives you long-term growth that can sustain you for many years to come.

The ‘stereotypical’ retirement allocation between aggressive and conservative is 60/40. Meaning 60% aggressive and 40% conservative. This ratio isn’t perfect for everyone but it can be helpful to know what many other retirees are doing.

Conclusion

It would sure make my job a lot easier if there was a one size fits all approach to TSP investing in retirement. But there simply isn’t.

Everyone has different plans/goals for their retirements and your TSP investments need to be aligned with that in order for you to get the best results.