A common question among federal employees is, “when is the earliest I can retire?” It would be great to have a simple answer to that question. Federal employees have the ability to retire at many different ages depending on their years of service and what benefits they prefer to have in retirement. Here a list of different retirement types:

Full Retirement

The first and most preferable retirement option is called a “full retirement”. A full retirement means having the ability to get most or all the retirement benefits possible including a pension, health insurance (FEHB), life insurance (FEGLI), dental/vision, and possibly the FERS supplement.

The three ways to get a full retirement are the following:

Age 57 with at least 30 years of service

Age 60 with at least 20 years of service

Age 62 with at least 5 years of service

So, if you’re looking to retire as soon as possible with a full retirement and you have 30+ years of service, age 57 would probably be the best option. One of the best benefits for having a full retirement before the age of 62 is the FERS supplement. From your retirement until age 62 you will receive a monthly payment that is supposed to help out while you’re not eligible for social security.

Early Out Retirement (VERA)

VERA stands for Voluntary Early Retirement Authority. VERA can only be possible for someone if their agency offers it. It occurs when an agency wants to downsize or get rid of certain positions. With the approval of OPM, it can offer VERA to qualified employees for the early buyout. Your agency can’t offer VERA to just anyone, you have to be eligible. Here is what makes you eligible:

Be at least 50 years old with at least 20 years of service

Or, have at least 25 years of service at any age

With VERA, you can start receiving your pension immediately. You will also be able to receive health insurance (FEHB) and life insurance (FEGLI).

Remember, VERA is not a very common option. It only becomes available when/if your agency offers it. So, planning on VERA to retire early is NOT a great plan.

MRA + 10 Retirement

There could be many reasons for an MRA + 10 retirement. MRA stands for minimum retirement age. While some federal employees are just tired of their job, others want to focus on their families (kids/grandkids), and others are just dying to travel the world. Whatever the reason, these people are willing to sacrifice a few benefits to retire earlier.

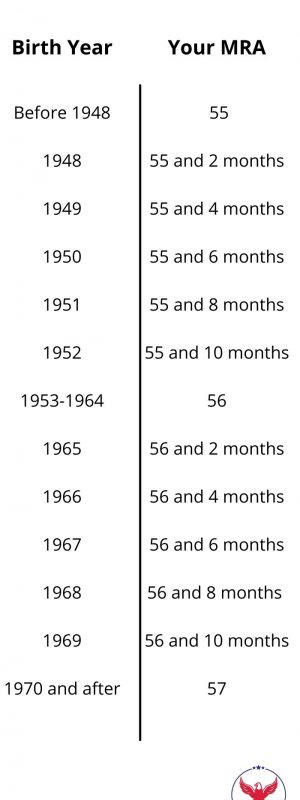

Most people’s MRA is at age 57. But, there are a few exceptions based on what year you were born. Here is a chart of what your MRA is:

If you’ve reached your MRA and have at least 10 years of service, you qualify for this type of retirement. You may ask yourself, “Do I get all the benefits of a full retirement?” and the answer is “mostly”. For every year you retire before age 62, you would get a 5% reduction to your pension.

Example: If you retire with an MRA + 10 at age 57, your pension would be reduced by 25% (5% x 5 years).

With an MRA + 10, you are still eligible to receive health insurance (FEHB), life insurance (FEGLI), and dental/vision into retirement. Also, keep in mind that with less years of service, the pension overall will also be less.

If you are looking for an MRA + 10 retirement and you don’t want a pension reduction, you can look into a postponed retirement.

Postponed Retirement

A postponed retirement is when you retire with the MRA + 10, but you decide to not receive your pension, health insurance, or life insurance until you turn 62. This allows you to avoid the 5% pension reduction for every year you retire before the age of 62.

For some people their pension is very important to their retirement and so a postponed retirement might be the best option. But, trying to replace the missed pension and benefits until you turn 62 can be a challenge.

After a postponed retiree turns 62, they would receive their whole pension benefit and be eligible for health insurance (FEHB) and life insurance (FEGLI) once again.

Deferred Retirement

This is probably the easiest retirement to qualify for. But, you lose many of your benefits. To qualify, you must have at least 5 years of service and leave your contributions into the FERS system. So, what does that mean?

Basically, every paycheck you contribute a percentage of your pay into the FERS retirement system. Later, this system will be what funds your pension in retirement. However, if you leave federal service early you will have the option to get a refund of everything that you contributed into this system. But, as stated above, if you do take the refund then you will NOT be eligible for a deferred retirement.

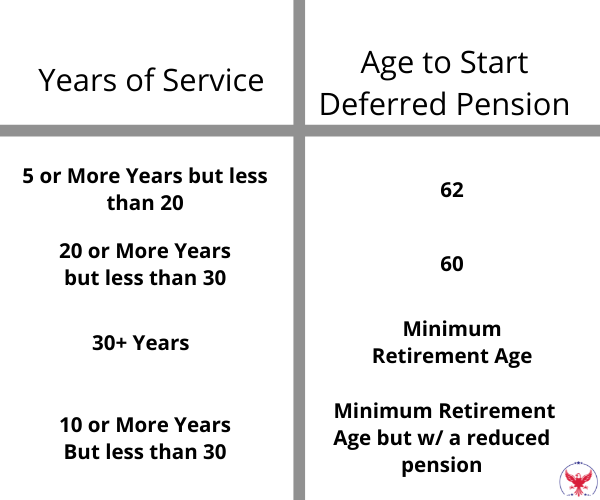

With the deferred retirement, you cannot receive health insurance (FEHB) or life insurance (FEGLI) or the FERS Supplement into retirement. However, you will be able to receive your pension at a deferred time depending on your years of service. Here is a chart on when you could receive your deferred pension:

Summary of Traditional FERS

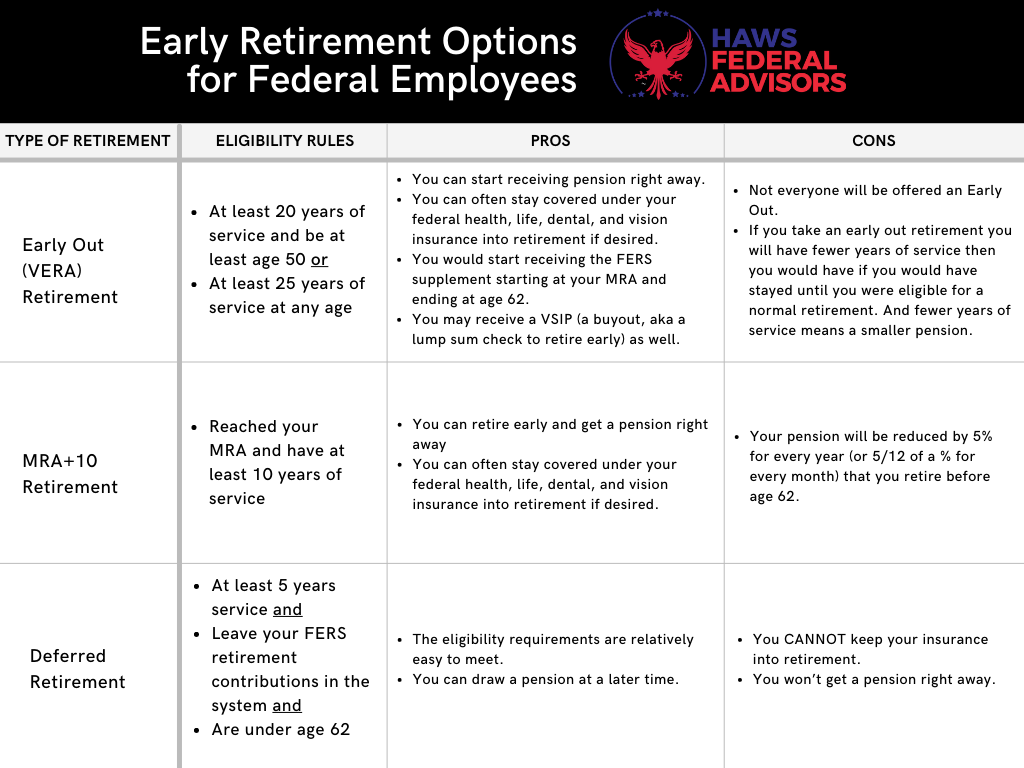

To summarize what we’ve talked about, here is a great chart that explains each early retirement:

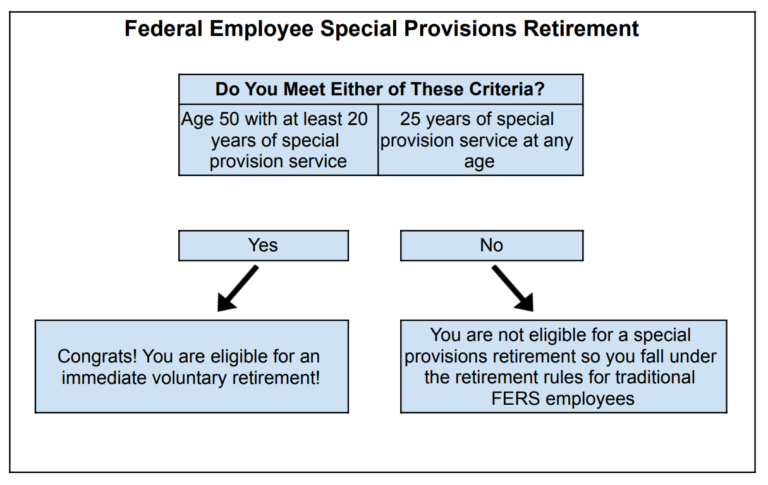

For Special Provisions Employees

Special provisions employees are able to have a full retirement a little differently than traditional FERS. You can either retire at age 50 with at least 20 years of service or retire at any age with at least 25 years of service. If you do not qualify for a full retirement, the options available to you for retiring early are the same as traditional FERS employees.